Japan Airlines and All Nippon Airways: Questions of fairness

September 2012

Japan’s two leading carriers have had a great year with record profits, successful launches of LCC subsidiaries (Peach, Jetstar Japan and AirAsia Japan) and exciting new growth with 787s. In recent months they have raised a combined $10.8bn on the stock market. But Japan Airlines (JAL) and All Nippon Airways (ANA) face a tougher future, with escalated competition from all quarters and worsening macroeconomic malaise. There is also the thorny question of how the inequalities resulting from JAL’s revival might be addressed.

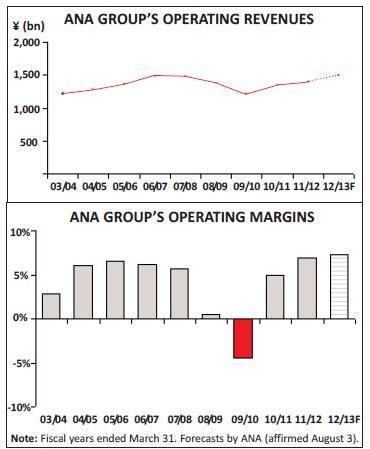

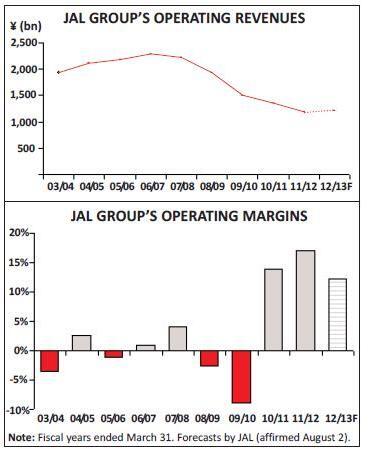

JAL and ANA have come a long way in the 18 months since the devastating March 2011 earthquake, tsunami and nuclear accident in north-eastern Japan. Surprisingly, both airlines posted record operating profits for their fiscal years ended March 31, 2012. ANA’s operating margin was a healthy 6.9%. JAL’s 17% margin – a result of its hugely successful restructuring in bankruptcy – made it one of the world’s most profitable airlines in that period.

The Japanese carriers have recovered so well, first, because business travel bounced back quickly (within months). Second, the airlines were helped by the fact that the Japan outbound travel market is twice as large as the inbound market even in normal times.

Third, the airlines did not fare too badly domestically because most regions in Japan were largely unaffected by the crisis (except for nationwide problems such as continued power shortages), because in the affected areas air travel was often the only possible mode of transport, and because the rebuilding efforts generated new travel.

Fourth, the airlines responded quickly with smart strategies. They slashed capacity, adjusted frequencies and aircraft sizes, stimulated leisure demand with discount fares, captured more international connecting traffic and operated special flights as part of support for rescue and recovery efforts.

So, for Japan’s airlines at least it was back to “business as usual” in record time. JAL and ANA have moved almost in tandem to implement the same strategies – with ANA being in the lead in part because JAL was earlier restructuring in bankruptcy.

Top projects at both airlines have included launching Japan-based joint venture LCCs, aimed at safeguarding their market shares in Japan and taking advantage of Asia’s enormous growth potential. ANA’s Peach Aviation took to the air in March, JAL’s Jetstar Japan unit in July and ANA’s AirAsia Japan in August.

Alliances have been another priority. Immunised joint ventures in the US-Japan/Asia market – JAL’s with American and ANA’s with United Continental – went into effect in April 2011. ANA was the first to implement a similar JV on Japan-Europe routes. The deal with Lufthansa was introduced in October 2011 and fully implemented in April; the airlines are now awaiting regulatory approval to add Swiss and Austrian to their JV. JAL and BA are preparing to launch their immunised Europe-Japan JV in March 2013.

This year has also seen new international expansion facilitated by the 787. ANA and JAL were the world’s first two operators of the type.

The Japanese carriers have even moved in tandem to tap the stock market for funds, albeit for entirely different reasons. ANA raised ¥182bn or $2.3bn (including overallotments) in a secondary share offering in July/August to fund its fleet plan and build cash reserves for possible future acquisi tions.

JAL’s shares were deliberately priced low to attract retail investors, which made up around 70% of the buyers. The price represented just 5.3 times projected 2012/13 earnings, compared to ANA’s 13-14 times in early September. JAL’s stock was much in demand. The international tranche (25% of the total) was six times oversubscribed, as foreign investors were attracted by the low valuation, clean balance sheet and high profit margins. The IPO was also a huge success from the government’s and taxpayers’ viewpoints: ETIC almost doubled its original investment. With a market capitalisation of ¥687bn ($8.8bn) when it was listed on September 19, JAL became the world’s fourth largest airline by market value (after Latam, Air China and SIA).

However, the stock made a weak debut, rising by only 1% on the first day. One concern has been that many of the retail investors may want to take profits in the short term. Like ANA’s, JAL’s shares offer domestic air ticket discounts of up to 50%, designed to persuade people to hold onto the shares longer, but that perk is becoming less attractive now that LCC service is more widely available in Japan. Furthermore, because of various economic, competitive and possibly political headwinds ahead, many analysts feel that the JAL shares are not attractive in the long term.

Multiple challenges ahead

JAL and ANA are likely to find the going getting tougher in late 2012 and in 2013. Internationally, growth and earnings prospects are not promising because of the lingering and possibly worsening European debt crisis and its effects on the global economy. Oil prices have risen again in recent months and the new tensions in the Middle East do not bode well.

Asia’s economic climate has deteriorated markedly in recent months. Growth is now slowing in China, a huge market that Japanese businesses depend on and one that ANA and JAL have been counting on for expansion. Japan’s exports to China already declined in June and July.

Mid-September saw another worrisome development: a sudden flare-up of the longstanding territorial dispute between China and Japan over a tiny group of uninhabited islands (known as Senkaku in Japan and Diaoyu in China). The anti-Japan sentiment and violent protests that have erupted in China have made life difficult for Japanese businesses and factories operating in China and dented the sales of their products. By September 21 cancellations by tour group passengers on Japan-China routes were running so high that the airlines slashed capacity in the market. JAL nearly halved its flights to Beijing and Shanghai through October 27 (and its newly listed shares tumbled). The crisis could blow over in a month or so, just like the previous flare-ups, or the economic impact could be severe and long-lasting.

One of the biggest challenges facing ANA and JAL is that Japan is now entering a new competitive era in terms of airline operations, thanks to a massive increase in airport capacity in the Tokyo metropolitan area in 2010-2013, many open skies ASAs signed in recent years that fully liberalise access to Tokyo from 2013, efforts by key airports to provide lower-cost facilities for LCCs and other policies that foster competition.

JAL and ANA were major beneficiaries of the initial Haneda “big bang” in October 2010, when maximum annual aircraft movements there increased by 43% and Haneda was opened to scheduled international flights. JAL and ANA have also received their fair share of new slots in the subsequent allocation rounds at Haneda, while gradually getting used to new competition at the airport. But the 2013 changes – notably a new terminal exclusively for LCCs at Narita and a 40% increase in Narita’s total slots – will benefit other carriers more, bringing a flood of new competition.

So internationally JAL and ANA will face sharply escalated competition from foreign operators, both established carriers and LCCs, on both short- and long-haul routes. Many of the new Narita slots will go to Asian LCCs, including SIA’s Scoot, AirAsia and Jetstar. Last year Narita was expecting seven or eight LCCs to use the new terminal when it opens in FY 2013.

Although the domestic market is large (83m passengers), it has stagnated in terms of full fare/business travel. The population is declining. There is fierce competition from Shinkansen bullet trains. Now, at the leisure end of the scale, the domestic market is seeing a new wave of new-entrant LCCs, keen to test if the market can be stimulated with low fares.

Of course, ANA and JAL are part-owners of three LCCs, which they smartly launched ahead of next year’s influx of competition. But many consider the joint-venture LCCs a risky strategy. While enabling the established carriers to retain some leisure market share, the LCC units will have a negative impact on the domestic pricing environment and may even poach higher-yield traffic from JAL and ANA in some markets.

Then again, as ANA and JAL executives have pointed out, if they did not do it someone else would. LCCs are expected to take the bulk of any incremental market growth to capture 17-20% of the domestic market this year. CAPA recently predicted that LCCs could account for half of all domestic seats in Japan by the end of the decade.

In the near term, the Japanese carriers have contrasting earnings outlooks. JAL faces many cost pressures after the sharp cuts in bankruptcy. Its labour costs will rise as bonus payments are restored (already taking place) and workers start demanding salary increases after the sacrifices made. Leasing and interest costs will soar as the 787 deliveries gather pace. But JAL is hoping to offset some of those hikes with a modest new ¥50bn ($638m) cost-cutting programme over the next five years.

JAL expects its operating profit to decline by 27% to ¥150bn ($1.9bn) and net profit by 30% to ¥130bn in the current fiscal year ending March 31, 2013. But the operating margin would still be a very healthy 12.3%. The goal is to achieve an operating margin of at least 10% in each of the next five years – something that would make investors very happy, especially if JAL keeps its promise of paying dividends of about 15% of net income.

In contrast, ANA is still poised to grow its earnings this year, because it has more scope to cut costs and because it is feeling pressure to narrow the profit gap with JAL. ANA has an ambitious new ¥100bn ($1.3bn) cost-cutting programme in place for the fiscal years 2012/13 and 2013/14, equivalent to a ¥1 reduction in CASK.

ANA expects its operating profit to increase by 13.4% to ¥110bn ($1.4bn) and net profit by 42.3% to ¥40bn in the current fiscal year. Operating margin would be 7.3%. The aim is to pay 25% of net income as dividends. The current corporate plan targets a ¥130bn operating profit (8.3% of revenues) in FY 2013/14 and “medium-term” operating income and margin greater than ¥150bn and 10%.

Questions of fairness

JAL’s outlook will also depend on whether there is a major shift in the political climate to favour ANA, after much criticism that the government showed JAL unfair favouritism when rescuing it and helping it turn around financially. There is an intense public debate on this subject in Japan, with ANA, opposition politicians and others arguing that the playing field is no longer level.

JAL’s net profits have been artificially boosted by the lower interest payments resulting from the more than ¥500bn ($6.3bn) of debt waivers granted by creditors in its bankruptcy and the lower depreciation costs following the write-offs of large numbers of its aircraft. JAL benefited from the massive funding from ETIC, which was formed essentially with the airline’s rescue in mind. But the biggest bone of contention are the $4.5bn tax credits tied to the reorganisation that, thanks to tax law changes in 2011, JAL can apparently use to offset corporate tax for up to nine years.

The US experience has shown that the Chapter 11-type process is profoundly unfair to competitors. It really creates an uneven playing field. The latest example is AMR, which had to file for Chapter 11 in the first place because it could not compete against all the other carriers that had slashed their costs, shed their pension plans and restructured their debt in bankruptcy.

In the Japan airlines’ case, the unfairness of the Chapter 11-type process seems magnified. First, there are only two large airlines. Second, the rescue involved taxpayers’ money. Third, the government went totally overboard helping JAL. Fourth, $4.5bn of tax credits following bankruptcy seems outrageous.

Therefore some form of redress seems appropriate and likely. ANA, which appears to have stepped up the fight after JAL’s successful IPO and listing, has called for political intervention to rebalance the competitive landscape, for example, through the allocation of domestic slots at Haneda. Favouring ANA over JAL in route/slot allocations is a potential solution that has been debated for years.

According to the Financial Times, ANA’s leadership argues that an airline that has failed should not immediately be given new slots, and that Japan should perhaps adopt rules similar to the EU’s “prohibiting an airline that has received public funds from using that money for anything other than restructuring”.

JAL: International growth

and alliances

JAL’s 14-month court-led restructuring (January 2010-March 2011) tackled its cost and balance sheet problems very effectively. The airline closed some 49 unprofitable routes, withdrew from 11 overseas and eight domestic destinations, shed more than 100 aircraft, slashed its headcount by about one third, switched to smaller and more fuel-efficient aircraft and rationalised the mainline fleet from seven to four types. The result was a dramatic reduction in operating costs: between 2008’s and 2011’s June quarters, as JAL’s ASKs fell by 43%, its total operating costs more than halved, leading to a 14.3% reduction in unit costs.

The restructuring also included selling many non-core businesses, updating JAL’s obsolete IT systems and changing from a rigid, multi-layer organisational structure to a more streamlined managerial framework. JAL continued cost cutting last year, and in April it put in place a new divisional profitability management system.

The turnaround was engineered and overseen by Kazuo Inamori, the 80-year old founder of electronics maker Kyocera and a management guru who took over as chairman when JAL entered bankruptcy. He trained JAL’s management to become more profit-oriented and to execute business plans more reliably. Inamori, an ordained Zen Buddhist priest, evidently succeeded in transforming JAL’s culture using somewhat unusual methods. He introduced a “JAL Philosophy” handbook that all 32,000 workers carry and discuss at staff meetings. The book teaches about cost-consciousness and includes mantras such as “be thankful”. According to press reports, after initially being sceptical many employees have been converted .

One obvious question is whether JAL can sustain the new culture after Inamori retires in early 2013. He loosened the reins in January when he became JAL’s “honorary chairman” and a new leadership team was named, with Masaru Onishi taking over as chairman and Yoshiharu Ueki as president. Ueki, an ex-pilot, was handpicked for the job by Inamori, though like Onishi he comes from the ranks of the old JAL management.

JAL’s post-bankruptcy strategy focuses on its traditional strengths: the business travel segment and the key global, regional and domestic markets that have high volumes of business traffic. That means a network centred on major US and European cities and the high-growth Asian routes. Long-term strategy includes major expansion of international flights at Haneda and strengthening Narita’s role as a global hub between North America and Asia. Domestic strategy focuses on maintaining a network centred on Haneda, and to a lesser extent Itami (Osaka), and operating more frequent service using smaller aircraft. JAL no longer operates freighters. The network is nicely balanced with domestic passengers accounting for 48.5% and international passengers 42.9% of air transport revenues in the June quarter (cargo accounted for the remaining 8.6%).

After the drastic contraction in bankruptcy, JAL is now resuming modest growth with the help of the 787 and global alliances (Inamori is known to worry about over-ambitious expansion). JAL’s five-year plan for the 2012-2016 period anticipates ASKs increasing by just 13%.

JAL deployed its first 787s in the lucrative business-oriented Narita-New Delhi, Narita-Moscow and Haneda-Beijing markets and to launch a new Narita-Boston route in April. Narita-San Diego will follow in December and Narita-Helsinki in March 2013. This autumn JAL is also using the 787 to boost service in the Tokyo-Singapore market.

Boston and San Diego are JAL’s seventh and eighth US gateways. The new services represent those cities’ first direct links with Asia. They are examples of the types of large secondary markets – ones that bypass congested hubs such as JFK and LAX – that are now possible for JAL because of the 787 and the JV with AMR.

This strategy is not perfectly aligned with AMR’s “cornerstone” strategy, which among other things has meant a sharp contraction in Boston. But AMR’s partner JetBlue, which has developed a major business-oriented hub at Boston Logan, was there to help out: JAL and JetBlue forged a codeshare agreement that also covers JFK and helps feed traffic from all over the East Coast. Of course, both the Boston and San Diego routes are part of the JV with AMR.

Helsinki will be JAL’s first new European destination in 20 years. Currently JAL places its code on the well-established Helsinki-Tokyo A330-300 flights operated by oneworld partner Finnair. The attractions for JAL include Helsinki’s geographical location, Finnair’s extensive European network, a compact and well-designed terminal allowing for minimum connecting times as short as 35-40 minutes and already having Japanese signage, etc.

Alliances and JVs are especially important to JAL because of its earlier downsizing and because it is poised to grow at a slower rate than ANA. The restructuring plan called for “aggressive” utilisation of alliances and stipulated that JAL should also benefit from the “managerial know-how, facilities, IT systems and other tangible and intangible assets of alliance partners”.

JAL executives have spoken frequently about how the immunised JV with AMR has helped boost JAL’s competitiveness on the Pacific. North America-Asia (via Japan) joint fares have been offered since December 2011 and continue to be expanded. Narita-San Diego will be the 11th transpacific route covered by the joint venture.

JAL is now hoping to repeat those benefits in the Japan-Europe market with the immunised JV with BA. As the initial step, in October the two are expanding their existing codeshares (23 beyond-London routes and eight beyond-Narita segments) to cover the Narita-Heathrow route. Both will place their codes on the daily flights each of them operates, plus on BA’s five-per-week Heathrow-Haneda services. They will also offer joint fares.

In the past 12 months, JAL has also launched codesharing with oneworld members LAN, Malaysia Airlines (joining this winter), airberlin and NIKI, as well as WestJet through Vancouver. Qantas’s recent decision to loosen ties with BA and outsource its European flying to Emirates is unlikely to negatively impact JAL; Qantas’s leadership has stressed that the airline still wants to enhance ties with oneworld members such as Latam, AMR and JAL.

Curiously, in the publicly released version of its latest five-year plan JAL did not even mention its new 42%-owned LCC unit Jetstar Japan, a joint venture with Qantas’s Jetstar and the Japanese trading house Mitsubishi Corp. This may be partly because its Australian partner is responsible for the unit’s strategy (JAL has reportedly given it considerable freedom) but also because JAL wants to distance itself from the budget brand. The five-year plan stressed the need to “enhance the JAL brand” to emphasise things like “JAL’s distinction as a high-quality, full-service airline with a comprehensive international and domestic network” that are “setting it apart from LCC brands”.

Jetstar Japan began operations on July 3 with three A320s linking Narita, its first base, with Sapporo, Fukuoka and Okinawa. The airline will also operate from Osaka and is planning international service from first-half 2013 to leisure destinations in countries such as China, the Philippines, South Korea and Taiwan. Its fares are 40-50% lower than existing fares. CEO Miyuki Suzuki (former EVP at Japan Telecom and a female) was recently reported saying that Jetstar Japan could operate 100 aircraft by the end of the decade and about a third of its capacity would be international. The fleet will later include A320neos and possibly larger aircraft types .

JAL’s five-year plan for 2012-2016 envisages a ¥478bn ($6.1bn) investment in fleet, but it will mainly be for replacement. The figure includes the 20 orders placed in February for the larger 787-9 (of which 10 were conversions from earlier 787-8 orders), for delivery from FY 2015. The 787-9 offers 50 more seats and is therefore part of JAL’s arsenal to try to keep unit costs in check. JAL has now ordered 45 787s, including 25 787-8s and 20 787-9s, plus 20 options.

One question still open is whether JAL will get the desired long-term strategic shareholders. Inamori has repeatedly expressed a wish that BA and AMR would consider buying small stakes in JAL. The partners are probably willing, though they would prefer not to and must be hoping that institutional investors can fill the role of bringing long-term stability to JAL, like they do at ANA and other airlines.

ANA: Maybe also acquisitions

ANA’s key goals for the next two years are to adopt a “multi-brand strategy”, switch to a holding company structure and achieve cost savings and efficiency improvements. ANA will “leverage its strengths as a network carrier”, accelerate international expansion and improve profitability. The two-year plan for fiscal years 2012/13 and 2013/14 envisages a 22% capacity increase — much greater than JAL’s planned growth.

The two-year plan is designed, first, to strengthen ANA against a backdrop of global economic uncertainty, the European debt crisis, high oil prices and fluctuating foreign exchange rates. Second, it will help ANA become “Asia’s Number One” airline and fend off a new wave of competition. Third, it will help ANA take advantage of the expansion of airport capacity in the Tokyo metropolitan area, ANA’s role as the 787’s launch customer and the immunised JVs.

Like JAL, ANA is striving to clearly differentiate the products and services offered by the “mainline full-service airline” from the LCCs. The two-year plan also talked about prioritising punctuality and on-time performance and using a brand concept called “Inspiration of Japan” to try to acquire a “five-star airline rating from Skytrax” (a well-known airline and airport review and ranking website).

However, ANA holds majority stakes in its LCC ventures, so rather than distancing itself from the units (like JAL), ANA is switching to a holding company structure from April 2013 to make it easier to support different autonomously managed brands (ANA, ANA Wings, AirAsia Japan, Peach Aviation, etc.).

This is another indication that ANA is seriously interested in acquisitions. When completing the secondary offering in the summer, the airline said that the funds would “help take advantage of opportunities if they arise”. Bloomberg quoted an ANA executive saying: “We’re always looking at ways to expand and take more of the expanding market in Asia”.

Peach Aviation, ANA’s JV with Hong Kong-based First Eastern Investment Group and other investors, began operations with leased A320s in March, initially serving Sapporo, Nagasaki and Kagoshima from its Kansai (Osaka) base, which benefits from special lower-cost facilities for LCCs. International operations, launched in May, extend to Seoul, Hong Kong and Taipei (the latter from September 30). ANA recently disclosed that Peach hopes to make an annual profit by its third year.

ANA’s other (51%-owned) joint-venture LCC, AirAsia Japan, launched A320 operations in early August, serving Chitose, Fukuoka and Naha from its Narita base. International operations to Seoul and Busan will follow in October. The airline may establish another base at Nagoya and could serve Taiwan and China in the future. It will benefit from the successful business model and well-known brand of AirAsia.

ANA is clearly confident of making the dual-LCC strategy work. Tokyo and Osaka are different markets, but eventually the strategy will limit Peach’s and AirAsia Japan’s growth. Then again, ANA has indicated that its priority is to cover as many future LCC markets as possible.

After debuting the 787 on domestic routes in November 2011 and subsequently on Haneda-Beijing, ANA used the aircraft to launch Haneda-Frankfurt in January. This autumn is seeing the 787 deployed in a wider range of domestic and regional markets and to upgrade Narita-Seattle in October. In January ANA will use it to launch a new Narita-San Jose route. Frankfurt and San Jose are examples of new routes that are only possible with the 787. ANA has seen higher than normal load factors on the 787s, indicating its popularity.

Including exercised options announced on September 21, ANA has now ordered 66 787s, of which 36 are 787-8s and 30 are 787-9s. The airline expected to have received 15 787s by the end of September. Many of the 787s are for replacement of 767-300s internationally and 747-400Ds and A320s on domestic routes.

ANA executives said this summer that although the European routes were still profitable, the main focus continued to be on the transpacific market, especially to build the North America-Asia (via Narita) corridor with the help of the immunised JV with UAL. This will mean two new Asia routes, Narita-Yangon (Myanmar) and Narita-New Delhi, in October.

ANA is also counting on being able to expand the immunised JV with Lufthansa to meet the 22% international growth target in 2012-2013. Adding Swiss and Austrian to the joint venture would increase the Japan-Europe JV routes from seven to nine and within-Europe JV routes from 208 to 320.