China's Big Three - The rise of competition

September 2005

The Chinese government is increasing the pace of aviation liberalisation, but as competition increases and fuel prices rise, the Big Three airlines — Air China, China Eastern and China Southern — are facing a difficult year.

Although the Big Three all saw an improvement in financial results in 2004 compared with SARS–affected 2003, many analysts believe this year’s figures may be disappointing. The major reason for this pessimism is rising fuel prices — the government regulates fuel supplies in China, with the result that it is up to 20% more expensive than on the global market. In addition, the government has (so far) barred Chinese airlines from levying fuel surcharges. China Southern and China Eastern in particular could both could plunge into a loss this year as a result of rising fuel prices, and both airlines' shares have fallen by almost one–third so far in 2005 (although Chinese airlines tend to perform better in the second half of the year than in the first, so share prices could recover).

While the Big Three airlines hope higher fuel prices are a short–term phenomenon, of much greater impact in the long–term will be the effect of increasing competition — both between themselves, from the first handful of Chinese LCCs, and from increasing competition from foreign airlines such as Lufthansa and United.

This rise in competition is part of the increasingly liberal (or, more accurately, less state–controlled) aviation policies from the Chinese government, due partly to increasing pressure from the US and the EU, and partly to the need to be prepared for the 2008 Beijing Olympics. Now that the government has completed the restructuring of the aviation industry it launched four years ago (which involved the Big Three swallowing up many smaller airlines), it has started to examine other areas. Liberalisation has included:

- Allowing the Big Three to challenge their rivals at their home hubs.

- Giving Chinese airlines greater freedom to reduce fares.

- Examining the extension of an open skies policy that was introduced successfully in the Hainan region in 2003 into other provinces.

- Allowing the first direct flights between China and Taiwan for more than 50 years.

- Signing more liberal bilaterals; for example, a bilateral with the US in 2004 allowed two new airlines — Continental and American — to join existing US carriers United and Northwest on routes to China.

- Agreeing to negotiate later this year with the European Commission on a pan–European air services agreement that would replace 22 existing bilaterals with EU counties (many of which have been signed in the last two years and have allowed new direct services into China).

The start-ups

In addition, the government has agreed to allow start–up carriers in China, and so far four have launched or are in the process of launching. These are:

- Okay Airways, based in Tianjin and which started domestic charter operations in March with a 737–900 on lease from Korean Air (which intends to buy a stake in Okay).

However, Okay’s plans to offer low fares have apparently been hit by high landing fees out of Tianjin.

- Shanghai–based Spring Airlines, owned by a Chinese travel agency and which aims to become China’s first LCC after launching domestic routes in July with an A320 leased from GECAS. Spring offers a no–frills service, only offers seats via the internet and has plans for a fleet of 15 aircraft by the end of 2008. However, reports out of China indicate that it is having to increase its fares after protest from other airlines,

- Chengdu–based United Eagle Airlines, which launched its first domestic route in July using the first of four A320s it plans to lease from GECAS.

- East Star Airlines, based in Wuhan and owned by tourism group China East Star and which will launch routes to domestic destinations including Beijing, Shanghai and Guangzhou this autumn using 737s or A320s.

Government policy

- Shanghai–based Eastern Express, a scheduled, charter and cargo carrier that has yet to announce a launch date but which is owned by a syndicate of Chinese firms. Despite these developments, there is still a long way to go in the government’s liberalisation drive. For example, foreign airlines are not allowed to own more than 25% of a Chinese carrier, while late last year the government capped deliveries of new aircraft to China in 2005 to 147 in order to allow airlines time to "improve safety standards" — although this will not halt the boom in the fleet as it applies for one year only.

More seriously, the government needs to increase the pace of infrastructure improvements. Aircraft movements at Beijing airport, for example, will rise from 680 a day today to a forecast 1,920 a day by 2023.

But even the governments current plans to build 55 more airports in China by 2020 may not build up infrastructure capacity quickly enough. And there are growing problems with recruiting enough skilled staff. According to the Civil Aviation Administration of China (CAAC), China needs 12,000 new pilots in the next eight years, and already a shortage of pilots has forced some airlines to recruit from abroad. Shanghai Airlines is one of several carriers that have delayed taking delivery of new aircraft due to personnel shortages.

And China is still under pressure (particularly from the US) to revalue the yuan significantly.

It was fixed at 8.28 yuan to the US dollar until July, when it was revalued to 8.11 after being pegged to a basket of currencies. Although the move was a symbolic first step towards a free float, the US wants a much greater appreciation. Revaluation broadly benefits the Big Three as their financing and operating costs fall. China Eastern, for example, calculates that it will save between $12m and $18m a year in interest on its debt for every 1% that the yuan appreciates, while in June Deutsche Bank estimated that a 5% revaluation of the yuan would increase China Eastern’s 2005 pre–tax earnings by 235%.

In relative terms, however, concerns about rising fuel prices, increasing competition and inadequate infrastructure are insignificant given the continuing confidence about the prospects both for the Chinese economy and the aviation market in the long term.

China’s GDP has grown by 8.6% on average each year for the last decade, and according to the CAAC passengers carried in China rose 39% last year, to 120m, of which 100m were domestic. Yet the potential of the domestic market remains huge — whereas every US citizen makes, on average, 2.2 air trips every year, the figure for Chinese citizens is just 0.06 trips per year. Of course, the majority of China’s 1.3bn population are rural and are unlikely to be able to afford to travel by air even in the long–term, but according to the Chinese government around 250m Chinese are classified as having a "middle–income", defined as households with between $18,000 and $36,000 of assets. That’s 19% of the overall population, and this figure is forecast to rise to 40% by 2020. More importantly, today 50% of those living in China’s cities are already in this middle–income category, and thus the prime target market for Chinese airlines.

Domestic air travel has multiplied 20 times between 1980 and 1998, at an average growth rate of 16.5% per year, and Ma Xulun, the president of Air China, expects Chinese air travel to rise by up to 15% a year for the next five years. And while there were 1bn train journeys in China last year, most of these were local, as with distances being so great in China high–speed trains do not provide the same competition that they do, for example, in Europe. A Beijing–Guangzhou HST service would take 9 hours, for example.

On top of the domestic market, there’s also huge potential for overseas travel. According to the World Travel and Tourism Council, more than 100m Chinese will travel internationally each year by 2020. International travel demand out of China has been reigned back by the government’s restriction on countries that its citizens are allowed to visit (the so–called Approved Destination List), but that number now stands at 55 after 27 European countries were added to the list last year.

The Chinese fleet

The Big Three airlines (excluding non integrated partners) continue to dominate the Chinese fleet, accounting for a substantial 66% of the total mainland Chinese fleet in 2005. This continues the increase in fleet share seen in the 2000s, from a low of 36% in 2002. In absolute terms the Big Three now operate 545 aircraft, a 40% increase from 390 aircraft in 2004. And despite the rise in start–ups, the Big Three’s dominance is set to continue as they currently have 162 aircraft on order, out of total outstanding Chinese fleet orders of 227 aircraft. That compares with just 63 orders 12 months' previously, and is an indication just how much of an emphasis the Big Three have put on expansion over the last year.

Boeing accounts for 568 aircraft (or 58%) out of the total Chinese fleet, with Airbus having 295 aircraft (30%) and others 113 aircraft (12%). Airbus has 162 outstanding orders in China, more than doubling its order book in the last 12 months. 107 of them are for A320 family aircraft (with 50 of them being made in the last 12 months) and 48 are for the A330 (35 in the last year).

In contrast, Boeing’s order book has inched up (in relative terms) from 58 aircraft in 2004 to 64 in 2005. All but seven of Boeing’s outstanding orders are for 737NGs. However, Boeing’s position will be strengthened considerably when part of a framework order for up to 60 787s from Chinese airlines is firmed up (due as Aviation Strategy went to press).

For the moment, 737s continue to be the dominant type in the overall Chinese fleet, with 330 aircraft (34%), followed by the A320 family with 186 aircraft (19%), though again, this gap is narrowing as the older 737s are retired and Airbus’s dominance in new short–haul aircraft orders is reflected in the delivered fleet.

According to Airbus’s latest forecast (released in December 2004, in which it devotes no less than seven pages to the Chinese market), Chinese airlines will need 1,790 new aircraft over 2004–2023, worth an estimated $242bn in 2004 dollars. That’s a huge uplift on Airbus’s forecast a year before, when it forecast 1,530 new aircraft worth $176bn over the following 20 years.

Airbus’s emphasis on China contrasts with Boeing, which — frustratingly — omits any specific mention of estimated aircraft orders for China in its latest forecast, released in June 2005. Boeing previously broke down forecasts orders by countries, but this year has kept figures at an aggregated, regional basis (i.e. China is rolled into the Asia–Pacific region aircraft forecast). Curiously, even Boeing’s own China website contains a "Boeing and China pamphlet" that dates back to 2002 and talks about forecasts for the years 2001–2020. Hopefully, Boeing’s sales presence on the ground in China is better than its current marketing collateral. Boeing has also been hit by US trade policy, whereby tariffs on exported aircraft parts have led to rising maintenance costs for Chinese airlines that have large Boeing fleets (which is most of them). In an attempt to mitigate the effect of this politically, earlier this year Boeing signed contracts worth $600m with Chinese manufacturers to build parts for its 737 and 787 programmes. Airbus also allows local manufacture of A320 components, and is likely to agree a similar tie–up for A350 production.

Air China

Beijing–based Air China, the national flag carrier, operates a fleet of 143 aircraft to more than 115 destinations, of which one–third are international.

Air China is also the largest cargo airline in China, owning 51% of Air China Cargo,Air China has traditionally been seen as the weakest of the Big Three, due to perceived government interference, but that view appears to be changing now that it has finally joined its main rivals by listing on the London and Hong Kong stock exchanges (after three previous postponements in the 2000s) in December 2004.

Advised by Merrill Lynch and China International Capital Corp, Air China was successful in selling 31% of its equity and raising $1.1bn. Air China is using $580m of the IPO proceeds to fund the purchase of aircraft, while the rest is to pay off long–term debt. The retail part of the float was oversubscribed 83 times and the institutional part 40 times, and as a result of overwhelming demand the retail share was increased from the planned 10% to 40%. Institutional investors bought 27.5% of the float, while Cathay Pacific acquired 32.5%, giving it a 9.9% share of Air China overall.

Although Air China listed at a discount to its two rivals (it was priced at a forward P/E ratio of 10.9, compared with 11.4 for China Eastern and 14.5 for China Southern), Air China’s market capitalisation is now approximately $3bn — higher than China Eastern ($1bn) and China Southern ($1.7bn) — and some analysts now consider Air China as a better long–term bet than its two rivals.

Part of that optimism stems from the benefits Air China will receive from the Beijing Olympics of 2008. The airline currently accounts for just under 50% of all traffic to/from Beijing, and will get a huge boost to its revenues from the event. In preparation, Air China plans to expand its fleet by almost one–third by 2008, and these may include two leased A380s, which Air China is believed to be negotiating with ILFC. Aircraft currently on order include 15 787s (due to be confirmed), 10 A320 family aircraft and 16 737NGs. In January this year Air China also ordered 20 A330–200s, for delivery in 2006- 2008 and worth $2.9bn at list prices. They will partly replace existing aircraft and partly be used for new long–haul routes.However, the Olympics also represent a threat to Air China, as they are attracting even greater interest in the Chinese market from foreign airlines. More than 80 foreign airlines currently operate into China, and that figure is rising. In an effort to combat this Air China is investing $83m in renovating its first and business classes on 15 long–haul aircraft by the end of 2005.

Air China is also in negotiations to join Star, which has long been seen as a natural global alliance for the airline, although new minority holder Cathay Pacific, a member of oneworld, may complicate the issue. Cathay chairman David Turnbull joined the Air China board in May, the two airlines will link their FFPs in the third quarter of 2005, and later in the year they will begin code–sharing between Beijing and Hong Kong.

Earlier this year there was much speculation that the growing ties between the two would lead to a "mega merger" whereby Air China and Swire Pacific (owner of 46% of Cathay Pacific) exchange equity. Although this would give Air China access to better management expertise at Cathay, such a deal will be tricky both politically and in terms of regulatory issues, and such a possibility was denied by both airlines (although negotiations between the two were held).

Although it is likely that Cathay will buy a stake in a Big Three carrier at some time in the future, apparently a more likely deal in the short term is that Air China sells to Cathay its 43% stake in Hong Kong–based Dragonair (held via China National Aviation Company, of which Air China owns 69%). Cathay already owns 18% of Dragonair (which expanded its existing code–share deal with Air China this year) and may see control of the airline as the best way of expanding its network into China. Cathay operates to a handful of destinations in mainland China, while Dragonair has more than 20 routes.

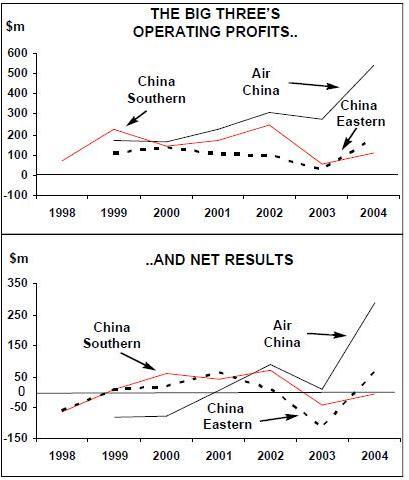

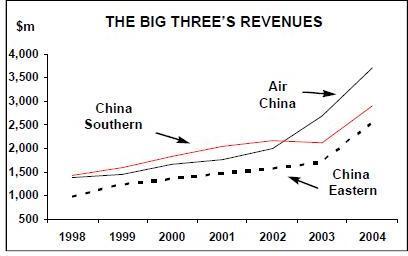

Even if a merger does not take place, closer Air China/Cathay ties are a serious threat to the other main Chinese airlines, as they provide a seamless connection for the large mainland–Hong Kong market. And Air China is also planning to open hubs in Shanghai and Guangzhou, the backyards of China Eastern and China Southern. Air China also recorded its best ever set of financial results in 2004, with a net profit of $289m (higher than forecasted in its own IPO prospectus), compared with just $11m in 2003, and based on a revenue of $3.7bn ($2.7bn in 2003). The airline implemented a series of cost cutting measures in 2004 (and aims to cut costs by $120m over the next three years), but the majority of the boost to its bottom line in 2004 came from substantial traffic increases on both international and domestic routes. Passengers carried rose 36% to 24.5m in 2004, with RPKs up by 39%, ASKs by 28%, and load factor rising to more than 70%. Although no financial figures are yet available for the first half of 2005, passengers carried in the period rose 13% to 12.6m, with load factor up by 3.3 percentage points to 71.9%.

Looking to 2005, Air China plans to distribute up to 30% of profits made this year as dividend to shareholders, while Air China is also issuing $423m of 10–year bonds this year to part finance the purchase of the A330–200s ordered in January. The aircraft will be used partly for an ambitious expansion of European services, where Air China plans to double frequencies within five years to all seven existing routes.

Air China is also looking to make further strategic acquisitions. It bought 23% of Shandong Airlines in February 2004 and in October last year Air China also purchased 51% of Air Macau, It is also reportedly negotiating with the Peruvian government to buy up to 70% of the TANS airline.

However, in May this year Air China lost out on its bid to buy a 65% stake in Shenzhen Airlines (in which it already has a 25% stake) after it pulled out in the 93rd round of an auction held by the Guangdong Development Bank. The airline is based in the south of China and operates 29 aircraft on more than 80 domestic routes. It is a regional competitor to China Southern, and its acquisition would have been a major boost for Air China. However, Air China pulled out after bidding $328m, leaving the winning bid to a joint venture from two investment companies — the Yi Yang Group and Huirun Investments — who offered $329m.

Shenzhen has 10 aircraft on order and ambitious expansion plans to build up a fleet of 100 aircraft within the next five years. It was the only Chinese airline to stay profitable through the SARS crisis, and in 2004 posted a net profit of $24m. Air China now says it will sell its 25% stake in Shenzhen.

Air China also faces bad news elsewhere. Although Air China hedged 25% of its fuel needs for international routes in 2004, as Chinese airlines are effectively not allowed to hedge fuel needs for domestic operations (thanks to a domestic monopoly supplier), rising oil prices meant that Air China’s fuel bill rose by 54% in 2004 to more than $1bn. Fuel accounted for 29% of operating costs in 2004, compared with 24% in 2003, but this year Air China has not been able to hedge any of its fuel costs, to the alarm of some analysts. Air China is lobbying the Chinese government hard to allow it to introduce a passenger fuel surcharge.

Another problem arose this summer when more than 400 travel agents in Guangzhou boycotted discounted tickets that Air China offered on selected flights (with fares up to 70% lower than normal) after coming under pressure from other airlines — including China Southern and China Eastern — which allegedly threatened to remove the agencies from their distribution networks.

China Southern

Guangzhou–based China Southern has the largest network of the Big Three, operating more than 300 routes to over 100 destinations with a fleet of 217 aircraft. This includes 66 737s and 46 A320 family aircraft, while on long–haul in June Southern received the last of four A330s it ordered in 2003 (it was the first Chinese airline to order and receive the type).

China Southern also has the biggest order book of any Chinese airline — 64 aircraft. In January it became the first of Big Three to order the 550–seat A380, and the first of five aircraft will arrive in 2007 (in time for the Olympics of 2008), with deliveries due to be completed by 2010. The aircraft have a list price of $1.4bn. In the same month China Southern provisionally ordered 13 787s, to be delivered from 2008 onwards, with three of them destined for Xiamen Airlines, of which it owns 60% (although there are unconfirmed reports that China Southern wants to reduce the number of 787s when the firm order is confirmed later this year.)

But the orders didn’t stop there. Earlier in the year China Southern agreed to lease five 737–700s, five 737–800s, five A320s and 10 A321s from ILFC, for delivery in 2006 and 2007, as well as nine 737–800s from GECAS, for delivery in 2005 and 2006. A deal for 23 leased A320s was also signed with ILFC at the end of 2004. The lease deals come as a direct result of the Chinese government’s restrictions on the overall amount of aircraft that Chinese airlines are allowed to import in any one year. Altogether, China Southern is committed to capex of $1.9bn in 2005 and 2006 alone — and in order to crew the expanded fleet, China Southern is also doubling its intake of trainee pilots every year to 250. The ambitious fleet expansion comes as China Southern is under increasing attack from its Big Three rivals. Guangzhou’s new Baiyun airport opened in August 2004 and is the largest airport in China, but both China Eastern and Air China have received permission to set up hubs there as well, while another airline — Shanghai Airlines — is also pressing the government to let it in.

That’s particularly worrying because of all the Big Three, China Southern is the most dependent on the domestic market, with 80% of revenue in 2004 coming from the domestic sector (compared with 54% at China Eastern and 39% at Air China).

However China Southern is trying to reduce its dependence on traffic in and out of Guangzhou. It already owns 49% of China Postal Airlines, 60% of Guizhou Airlines, 60% of Shantou Airlines, 39% of Sichuan Airlines and 60% of Xiamen Airlines, and in late 2004 it completed the purchase of China Northern Airlines and Xinjiang Airlines from its parent (China Southern Air Holding) for $2bn, as well as assuming $1.8bn in debt at the two airlines. This was part of the government’s restructuring of the aviation industry, and the acquisitions have boosted China Southern’s network in the north east and north west areas of the country respectively, where it previously didn’t have much presence. The acquisitions also boosted China Southern’s fleet by 70 aircraft, and will increase passengers carried at the airline to more than 40m a year (as well as extending the airline’s share of the domestic market from approximately 26% to 34%). China Southern is also counterattacking Air China by spending more than $130m on a new hub at Beijing, which will open in 2007.

China Southern’s international routes are focussed on the Asia–Pacific region, with a handful of routes to Europe and North America. But its international kudos was boosted considerably by the order for the A380s, which are both a symbolic and actual challenge to the traditional long–haul dominance of Air China, the only mainland Chinese operator of the 747–400. China Southern is also likely to become the first of the first of Big Three to join a global alliance,with SkyTeam membership likely in 2006. China Southern already has code–share or other links with KLM, Delta and Korean Air, and in April China Southern and Northwest Airlines started a joint marketing programme, including reciprocal FFPs. An FFP tie–up was also signed with Air France at the end of 2004; China Southern’s FFP — called Sky Pearl — has 2.5m members and is the largest of the Big Three. A joint venture between China Southern and Air France on France/China routes is also under negotiation. The international focus follows a surprising set of financial results for 2004.

Despite having a profitable first three–quarters of the year, China reported a net loss of $6m for 2004, less than the $43m loss of 2003 but a disappointment given that analysts were expecting a profit for the year. Fuel costs (which account for 30% of all costs) rose by 57% in 2004, but other costs rose too, largely due to expansion by the airline. Revenue rose 37% to $2.9bn in 2005, while operating profit doubled, to $110m. Passengers carried rose 38% to 28.2m, ASKs grew by 32% and RPKs by 41%, with load factor rising 4.6 percentage points to 69.2% in 2004.

Worryingly, China Southern stated that the "sustained high fuel price ... might climb even higher", and the airline is implementing various cost–cutting programmes in 2005. But with a larger domestic presence than its rivals, China Southern’s aircraft have fewer opportunities to refuel at overseas airports. Additionally, China Southern will have substantial costs from the integration of China Northern Airlines and Xinjiang Airlines into its operations.

Prospects for 2005 do not look good, as China Southern has just announced a net loss of $112m in the first half of the year (compared with a $33m net profit in 1H 2004). That was despite a 52% increase in passengers carried in the half year — with a 1.7 rise in percentage points in load factor, to 68.2% — and a 61% jump in operating revenue. But thanks to the substantial rise in fuel costs compared with January–June 2004, operating costs rose by more than 75%, and China Southern recorded an operating loss of $52m (compared with an operating profit of $93m in January–June 2004). The airline states that it "intends to meet the challenge of soaring fuel prices by using economies of scale and strict control over operating costs increases".

China Eastern

Shanghai–based China Eastern returned to the black in 2004 with a net profit of $62m, compared with a net loss of $115m in 2003, and an operating profit of $179m ($27m in 2003). Revenue was up 47%, to $2.5bn, with 17.7m passengers carried in 2004, 44.7% up on 2003. RPKs grew by 50.9% in 2004, well ahead of the ASK increase of 37.4% and resulting in a 5.9 percentage point rise in load factor, to 66.3%. The biggest growth was in international services, where RPKs leapt by 73.9% in 2004, while domestic RPKs were — in relative terms — up by just 37.2%. However, China Eastern also disappointed analysts after rising fuel costs (up by 78% compared with 2003) resulted in a set of results that were lower than the consensus forecast, despite the implementation of cost–cutting programmes. There is also increasing worry about the level of debt at China Eastern, which now stands at $3.8bn, giving it a gearing level of 82%. The debt level has risen considerably in recent times due to a substantial increase in the size of the fleet.

China Eastern currently has a fleet of 185 aircraft, and it has 52 more on order. In fact the increase in China Eastern’s order book has been staggering. In October 2004 it ordered 20 A330–300s — its single biggest order since 2002 — for 2006–2008 delivery and at a cost of $3.4bn. The aircraft will replace existing A300s and A310s. In December it ordered six 737–700s for 2006 delivery, in March this year it ordered five A319s for 2006–2007 delivery, and in April it ordered 11 A321s and four A320s for delivery in 2006- 2008. In January this year China Eastern also signed a framework deal for 15 787s, to be delivered from 2008 and part of the bulk order for 60 787s worth $7.2bn placed by China Aviation Supplies Import and Export Group.

For regional operations, five ERJ–145s were ordered in March at a cost of $110m, for delivery in 2005–2006 and to be built by Harbin–Embraer, the China–based joint venture company. Its fleet was also boosted considerably this summer when the airline completed the purchase of China Northwest and Yunnan Airlines from its state–run parent for a combined price of up to $119m (as well as taking on debt totalling $1bn). Some analysts criticised the move, claiming that China Eastern overpaid its parent given the amount of debt it was also assuming. However, as the move was the last part of the government’s restructuring of the aviation industry, China Eastern had little say in the matter.

The acquisitions more than doubled the number of destinations served by China Eastern (from 238 to 503), boosted the airline’s share of the domestic market from 19% to 23%, and increased its fleet by 64 aircraft, (overtaking Air China in fleet size). The two acquired airlines were an important boost to China Eastern’s domestic assets — China Eastern also owns 63% of China Eastern Airlines Jiangsu, 40% of China Eastern Airlines Wuhan and 70% of China Cargo Airlines.

But China Eastern is under attack at its main hub, Shanghai, into which Air China is now expanding. Additionally, China Eastern is vulnerable at Shanghai given that it has to transfer passengers between international flights arriving at Pudong airport and domestic flights operating out of Hongqiao. A solution will only be possible in 2008 when a second terminal opens at Pudong, which China Eastern plans to dedicate to domestic services.

But one piece of good news domestically came in April when China Eastern received permission from the government to set up a hub at Guangzhou’s new Baiyun airport, a direct challenge to China Southern. China Eastern continues to open up new international routes — services to London Heathrow and Vancouver were launched in 2004, and this year routes have started to Moscow, Bombay, Los Angeles and Dhaka in Bangladesh. Also in 2004 China Eastern opened a new international hub in the northeastern city of Shenyang, with eight routes to Europe, Asia and North America, all going via Shanghai. China Eastern also linked FFPs with Taiwan’s China Airlines in late 2004 — the first such cooperation between Mainland Chinese and Taiwanese carriers.

And China Eastern started code–sharing with Air Europa on the Spanish airline’s services between Shanghai, Beijing and Madrid in May this year. That follows the increase in permitted weekly flights between China and Spain from two to 21 at the end of 2004 — a sign that competition on many international routes will only increase.

China Eastern has held talks in 2005 with prospective strategic partners, although the airline refuses to confirm speculation that Singapore Airlines and Japan Airlines (with which China Eastern expanded an existing code–share this summer) are two of the airlines believed to be considering an investment.

The airline has a longstanding relationship with Cathay Pacific, but this is unlikely to result in an equity tie–up given Cathay’s investment in Air China, a move that according to Li Fenghua, Chairman of China Eastern, was "a little bit unexpected".

The cooling in the relationship is believed to have begun when Cathay Pacific became upset about perceived lack of support by China Eastern for Cathay’s attempt to win Chinese government approval to enter the lucrative Shanghai–Hong Kong route.

Significantly this may derail what been previously been thought of as China Eastern’s inevitable membership of the oneworld alliance (given its partnership with both Cathay and American). But there are few alternatives for China Eastern, given the likely tie–ups between China Southern and SkyTeam, and Air China and Star.

Despite a rise of 6% in passengers carried and 7.8% in RPKs during the first six months of 2005, rising fuel prices led China Eastern to post a net loss of $59m for the half year, compared with a $50m net profit in 1H 2004.

While revenue rose 9.4% in the period, operating costs rose by 19.2%, with fuel accounting for 32% of this (and rising by a staggering 41% compared with fuel costs in January- June 2004). The airline says the rise in fuel costs was "drastic" and that it faces challenges in the rest of 2005. Ominously, a Morgan Stanley report described prospects for China Eastern’s earnings this year as "dismal".

| 737-2/300 | 737-4/500 | 737NG | 747-2/300 | 747-400 | 757 | 767 | 777 | A300/ 310 | A320 family | A330 | A340 | A380 | MD11 | MD80 | MD90 | Russian | Other | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Air China | 33 | 29 (16) | 12 | 13 | 14 | 10 | 21 (10) | (20) | 6 | 5 | 143 (46) | ||||||||

| Air China Cargo | 4 | 1 (2) | 5 (2) | ||||||||||||||||

| Air Hong Kong | 9 (2) | 9 (2) | |||||||||||||||||

| Air Macau | 3 | 13 | 2 | 18 | |||||||||||||||

| Cathay Pacific | 7 | 25 | 16 (1) | 25 (4) | 18 | 1 | 92 (5) | ||||||||||||

| Changan AL | 4 | 2 | 6 | ||||||||||||||||

| China Cargo AL | (2) | 6 | 6 (2) | ||||||||||||||||

| China Eastern AL | 25 | 28 (8) | 3 | 16 | 69 (24) | (20) | 10 | 3 | 9 | 7 | 15 | 185 (52) | |||||||

| China Postal AL | 2 | 2 | |||||||||||||||||

| China Southern AL | 30 | 12 | 24 (11) | 2 | 29 | 10 | 6 | 46 (48) | 4 | (5) | 23 | 13 | 12 | 6 | 217 (64) | ||||

| China United AL | 6 | 2 | 2 | 9 (1) | 19 (1) | ||||||||||||||

| China Xinhua AL | 6 | 3 | 2 | 11 | |||||||||||||||

| CR Airways | 2 | 2 | |||||||||||||||||

| Deer Jet | 2 | 1 | 3 | ||||||||||||||||

| Dragonair | 4 | 1 | 17 | 12 (4) | 34 (4) | ||||||||||||||

| Guizhou AL | 1 | 1 | |||||||||||||||||

| Hainan AL | 5 | 7 | 17 (11) | 5 | (8) | 28 | 62 (19) | ||||||||||||

| Okay AW | 1 | 1 | |||||||||||||||||

| Shandong AL | 13 | 2 (5) | 10 | 25 (5) | |||||||||||||||

| Shanghai AL | 1 | 16 | 13 | 5 (2) | 1 | 5 | 41 (2) | ||||||||||||

| Shanxi AL | 3 | 1 | 4 | ||||||||||||||||

| Shenzhen AL | 9 | 19 (4) | 1 (6) | 29 (10) | |||||||||||||||

| Sichuan AL | 17 (11) | 5 | 22 (11) | ||||||||||||||||

| Spring Airlines | 1 | 1 | |||||||||||||||||

| United Eagle AL | 1 | 1 | |||||||||||||||||

| Xiamen AL | 4 | 6 | 13 (2) | 9 | 32 (2) | ||||||||||||||

| Yangtze River Express | 5 | 5 | |||||||||||||||||

| Total | 142 | 28 | 160 (57) | 15 | 41 (4) | 64 | 27 (2) | 36 (1) | 34 (2) | 186 (107) | 41 (48) | 34 | (5) | 7 | 26 | 22 | 26 | 87 (1) | 976 (227) |