Chinese "Big Three": handed pole positions

October 2002

China’s airline industry is undergoing major consolidation as a result of the Chinese government’s decision to drastically reduce the number of second- and third–tier airlines in the country.

The so–called "big three" airlines — Air China, China Eastern Airlines and China Southern Airlines — today operate more than a third of China’s civil aviation fleet (excluding Hong Kongbased Cathay Pacific and Dragonair, which are not covered in this survey) and hold two–thirds of the country’s outstanding new aircraft orders — but these proportions will rise further as consolidation occurs.

The potential for Chinese passenger growth is undeniably large. Of a total population of 1.3bn, only around 50m have ever flown, and the domestic market is forecast to grow by around 7- 10% per year according to most forecasts. In addition the tourist market to China is growing considerably, and business travel to/from China is also expected to keep increasing, particularly now that China has joined the WTO. In 2001 75.2m passengers were carried on Chinese airlines, according to the Civil Aviation Administration of China (CAAC), which forecasts that this will grow by just over 10% in 2002.

China’s existing airline/aviation infrastructure, however, can be described as poor. With more than 30 airlines and a relatively old fleet (although average fleet age has improved over the last five years as Airbus and Boeing orders have arrived), service levels are on the poor side, and questions have been raised about safety standards after a series of crashes.

These are issues that the CAAC has been concerned about since the 1990s, but decisions that affect a major industry in China such as aviation take time to be debated and approved. Now, however, the decision bottleneck seems to have been broken, ongoing developments at Bejing Capital International Airport and the need to sort out China’s economy before the 2008 Beijing Olympics are major factors, and China’s aviation industry is changing as never before.

In fact, the first signal of airline consolidation was given by the CAAC in 2000, when it said that nine airlines under its direct control should be taken over by the "Big Three". Under the consolidation plan, which has been firmed up over the last two years and which was formally approved by China’s government in January 2002, it is planned that Air China will merge with China Southwest Airlines and the China National Aviation Corporation; that China Eastern will acquire China Northwest, Great Wall and Yunnan Airlines; and that China Southern will take over China Northern and China Xinjiang Airlines.

Of these planned mergers, only China Eastern’s takeover of Great Wall Airlines has been completed, and it is could be another two or even three years until this consolidation is completed, according to aviation observers inside China. But by then, the Big Three will account for approximately 80% of all domestic passengers carried in China.

"Disorderly competition"

In a further move that will also boost the power of the Big Three, the CAAC announced earlier this year that "disorderly competition" would be eliminated by restricting the number of airlines allowed to operate flights between the three largest hubs in China: Beijing, Shanghai and Guangzhou (near Hong Kong) — where, respectively, Air China, China Eastern and China Southern are based. (These airports also account for almost 80% international traffic to/from China.)

From this summer only airlines based in those cities have been allowed to operate between them, thereby eliminating all services on these routes by the second–tier airlines based in other cities. Already, load factor and ticket prices on these routes are starting to rise. Volume growth has slowed slightly however, as the CAAC are being given an illustrated lesson in the price elasticity of demand. From this winter all other airlines will be completely banned from using these airports as transit points on internal flights, instead being encouraged to start short–haul feeder flights into these cities. In a very blunt way, CAACis encouraging the emergence of a hub and spoke network through China, whether the airlines (or customers) like this or not.

In a complementary move to consolidation, the Chinese government is also easing the limits of foreign ownership in Chinese airlines. From August 2002 foreign shareholders are allowed to increase their stakes in Chinese airlines up to a maximum of 49%, compared with the previous limit of 35% (although individual foreign shareholders are not allowed to hold more than 25% each). This was a move that had been discussed in government circles since 1995 when Hainan Airlines became the first Chinese airline allowed to have a foreign shareholder. However, the recent entry of China into the World Trade Organisation — which will inevitably lead to greater competition from foreign carriers at some point in the future — was the impetus for the CAAC to finally make these changes, and it is likely that further easing of ownership restrictions will come within a few years.

This easing of restrictions on foreign ownership is being closely watched by western airlines,as well as by Asian ones such as Singapore and Cathay. Many of the larger carriers have already held informal talks with the Big Three, and alliances such as Star and oneworld are eager to get the major Chinese airlines on board. China is a major gap in the alliances' global network, and the Big Three are expected to sign up with alliances sooner rather than later. (Interestingly, the 14 Star alliance airlines met in Shanghai in June this year.)

However, even after this round of reform and consolidation is completed there is still a long way to go, as airlines in China simply do not operate in the same way that airlines do in the West or the rest of Asia. Government control is far–reaching — minimum pricing levels are "sent" from the CAAC, and most costs are completely outside the airlines' control: for example, airlines are not allowed to hedge fuel costs. But in terms of pricing, at least, government control is not always successful. Many of China’s 5000+ authorised travel/ticket agents heavily discount air fares, a situation that has lead to an intense fare wars over the last few years. Coming on top of the general Asia–Pacific economic recession of the late- 1990s, discounting has significantly affected the Big Three’s (and others') financial results after a long period of steady growth through the 1980s and early–to–mid–1990s. Yet Chinese aviation has escaped relatively lightly from the effects of September 11. Domestic travel was unaffected, and while US traffic has been down, Sino–Asian passenger levels have remained intact. Overall therefore, 2001 was a reasonable year for the Chinese airline industry, with the CAAC reporting combined airline profits of $83m. (The CAAC forecasts 2002 will see combined profits of $120m-$240m.)

Discounting, and the resulting erosion of Chinese airlines' profits, has been one motivation behind the industry’s restructuring. (Other determining factors include insufficient asset use, high taxes and jet fuel surcharges) — although whether consolidation into a stronger Big Three will necessarily lead to less discounting and stronger financial results remains to be seen. It may be a long time coming, but when they are free of all artificial constraints the Big Three will compete among themselves and with new entrants as they see fit. The market forces that the CAAC is slowly unleashing may create a Chinese airline industry that few can contemplate today.

Nevertheless, once consolidation is completed, the Chinese government — via the CAAC — is likely to ease up price controls, or abolish them completely. Or, as one analyst puts it, if they don’t do this then all CAAC’s hard work in consolidating the industry and opening it up to foreign influence would be lost among the criticism it would inevitably receive for not abolishing price controls. Much depends on the future role and scope of the CAAC, which is also being reformed. The direct stakes that CAAC owns in Chinese airlines are likely to be moved to other government quangos, and airport management will be passed to local government, thus allowing the CAAC to concentrate on impartial regulation of the industry.

Currently the CAAC is composed of 24 regional administrations, or "fiefdoms" according to one analyst, but that will be cut back to six or seven regions, with — theoretically — much reduction of overmanning and bureaucracy, although not in the near term.

As for aircraft orders, Boeing and Airbus’s practice of bullish assumptions about CAAC orders to underpin aggressive global market forecasts now seems dubious. In February Liu Jianfeng, the CAAC minister, said that Chinese airlines would need far less orders than the manufacturers had been predicting, primarily due to existing overcapacity. Larger aircraft types are over–represented in China’s fleet, and they are often flown with sub–50% load factors — meaning that domestic routes are often unprofitable.

Liu added that unless there were persuasive arguments that each specific new aircraft would be beneficial to an individual airline’s profits, the CAAC would not authorise new orders. The days of block mega–orders from the CAAC, which are then apportioned out to China’s airlines, are gone forever. The current Airbus and Boeing forecasts are for between $140bn-$150bn worth of new aircraft orders out of China to the year 2020, but at this point it seems improbable that China’s Big Three — even though they will be massive airlines — combined with a host of second–tier carriers could sustain such an orderbook given the current market overcapacity.

China Eastern

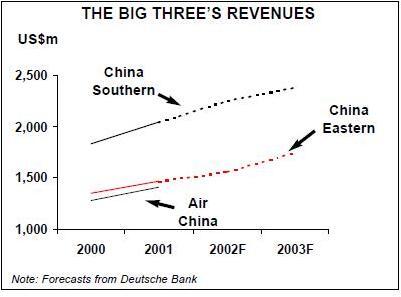

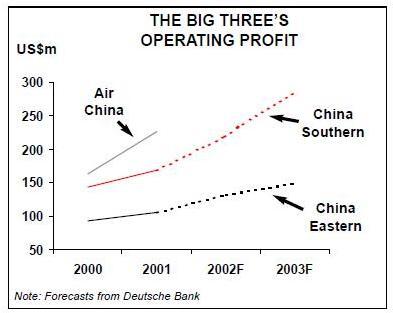

Shanghai–based China Eastern Airlines is going through a tough time at present, and the CAAC’s consolidation plans will — theoretically — provide much needed assistance to the Hong Kong–listed airline. In August China Eastern’s share price fell almost 10% after it revealed first–half net profits for 2002 of $3.1m, a fall of 64% compared with January–June 2001, due partly to the fare war that has broken out among China’s airlines and partly to forex losses. This result came despite a very favourable reduction in the tax rate payable by China Eastern in the period, with the Shanghai local tax authority reducing the airline’s tax rate from 33% to 15% from July 1 2001.

But China Eastern is pushing ahead with its long–term development plans, and in addition to the three airlines lined up by the CAAC for consolidation into China Eastern (China Northwest, Great Wall and Yunnan Airlines), in August China Eastern agreed to pay $29m for 40% of Wuhan Airlines. Wuhan is based in the Yangtze River basin and has a fleet of eight 373–300s and 800s.

It will now be renamed China Eastern Airlines Wuhan and will use China Eastern livery. Although Wuhan is small, the move is significant as the airline is not controlled by the CAAC, and shows that China Eastern at least is intent on hoovering up small, independent airlines in China. (China Eastern may also be exploring other acquisition options in the event that the CAAC consolidation plan does not take place — China Eastern is believed to be concerned about the level of debts run up by designated acquisition China Northwest.)

China Eastern is keen to expand its route network both domestically and internationally. Domestically, China Eastern is looking to expand routes in western China (a move encouraged by the Chinese government), while on international services the airline is increasing capacity on intra- Asian routes.

China Eastern, which employs 15,000 people, is regarded as lagging behind rivals in terms of operational, managerial and financial practices, but it is changing fast. Notable recent moves include:

- Devoting resources to enhancing its online booking facilities;

- Appointing independent directors to the board;

- Recruiting a US national to become Vice President US Sales (a significant move for a Chinese airline);

- Hiring South Korean flight attendants (China Eastern claims it is the first Chinese airline to hire foreign nationals);

- Agreeing a $2.1bn credit line with the Industrial and Commercial Bank of China until 2003, partly to pay for 20 A320s ordered in April (and which will be delivered in 2003–2005); and

- Changing its aircraft depreciation policy from 10- 15 years to 20 years, in order to bring its accounting practices closer to international standards.

Additionally, the airline is working hard to sign partnership airlines with foreign airlines.

China Eastern already code–shares with Air France and American, and started code–sharing with Japan Airlines in September. It has also maintained a close (but low profile) working relationship with Cathay Pacific and is part of Cathay’s “Asia Miles” FFP. Eastern is talking to other prospective code–share partners at present and is also believed to be negotiating with at least one of the major global alliances.

In terms of its fleet, China Eastern operates 67 aircraft, with 31 Airbus and Boeing aircraft on order (see fleet table, page 10).

Orders for up to 20 more aircraft (likely to be more short–haul models) are expected to come out of the airline in the next few months as it looks to increase capacity both domestically and internationally.

China Southern

China Southern Airlines is the largest of the Big Three, employing 19,000 people and with a fleet of 84 aircraft and 21 (all Boeing) on order.

Like China Eastern, Hong Kong–listed China Southern’s share price fell considerably in August after net profits dropped 39% in the first half of 2002, to $7.3m. Fare discounting hits yields badly, although in January–June 2002 domestic RPKs increased 16.1% and international RPKs 24.1%, compared with a total ASK rise of 9.8%.

Although international traffic held up well post- September 11, China Southern also noted that its aircraft insurance costs have increased by 45% as a result of the terrorist incident. According to Yan Zhi Qing, Chairman of China Southern, there will be a "challenging operating environment in the second half of the year", but the airline intends to keep on expanding its network domestically and internationally.

As well as the CAAC–designated takeover of Shenyang–based China Northern and Urumqibased China Xinjiang Airlines (which may not be completed until well into 2003), China Southern is pressing ahead with its own acquisition plans.

It has already bought a small carrier, Zhongyuan Airlines, and in June it agreed to pay $18m for 49% of China Postal Airlines (CPA), which operates all Chinese air postal services — (the other 51% will be remain with the China State Post Bureau.) However, despite its air post monopoly and its link–up with one of the Big Three, Tianjinbased CPA faces stiff competition from road and rail post services, which already account for the vast majority of internal China mail and freight.

The $18m purchase price for CPA was funded from China Southern’s cash flow, but the airline has also signed a $1.5bn credit line with the Bank of China, which will be used for other airline acquisitions and aircraft purchases. China Southern bought Sichuan Airline for around $17m in August. The carrier also plans to issue in A share (Domestic) market, although cash raised this way will go solely to aircraft purchases, specifically the 20 737–800s ordered in October 2001.

China Southern appears slightly more cautious about linking up with global alliances than its main rivals. Chairman Yan Zhi Qing has said that the fluctuating domestic market and need for intra–airline consolidation means that China Southern (or any other Chinese airline) is unlikely to join an alliance until 2004 at the earliest.

Instead China Southern will slowly build on existing relationships with airlines such as Delta and KLM — although if one of its rivals signs up with an alliance before 2004, China Southern may well be tempted to follow suit.

Air China

Beijing–based Air China — the country’s official "flag–carrier" — operates a fleet of 72 aircraft and has a further 15 on order. In 2001 the airline reported revenues of $1.4bn, 10.4% up on 2000, and a net profit of $5m, compared with a $78m loss in 2000. In January Air China cut 230 jobs as part of general cost–cutting — an unusual occurrence in China, let alone in the aviation industry — and is believed to have been as hard hit by the fare wars in China as have been the other members of the Big Three. But the airline still employs around 11,000 people and it is also believed to be carrying heavy debts, although the precise amounts are unknown.

The CAAC consolidation plan calls for Air China to merge with China Southwest Airlines and China National Aviation Corporation (CNAC), which operates CNAC–Zhejiang Airlines, after which China–backed conglomerate CITIC Pacific (based in Hong Kong, and which also owns holds 26% of Cathay Pacific and 29% of Dragonair) — is planning to buy a 25% in Air China. Unlike the other Big Three airlines, Air China is not listed, but will obtain a listing in Hong Kong or elsewhere once the mergers are completed. However, this plan may be running into trouble as CNAC is the commercial part of the CAAC, and unconfirmed reports state that CNAC and Air China are "discussing" just what kind of stake CNAC will have in the enlarged Air China once the mergers are complete.

Air China signed a wide–ranging alliance deal with Northwest Airlines in 1998, but reports suggest that this partnership may be waning due to Northwest dropping non–stop services between China and the US over the last year. Northwest’s decision has prompted Air China to start non–stop transpolar services between Beijing and New York in late September, but may also be encouraging Air China to look elsewhere for alliances.

The most likely candidate appears to be Star, as Air China has been in a code–share with Lufthansa for a couple of years already, and United are rumoured to want to sign an alliance with Air China if the Northwest deal fades out.

Air China has significant plans for cargo, and believes the immature domestic and intra/extra- China cargo market has great potential. The airline is aware that China Southern has bought into China Postal Airlines, while China Eastern owns 70% of international operator China Cargo Airlines. Air China may therefore spin–off its existing cargo operations (four 747–200Fs) into a new Beijing–based airline owned jointly with the CITIC Pacific, and discussions are believed to be taking place at present.

The airline recently cancelled an existing order for eight A318s, instead replacing them with orders for A319s, which will start arriving in June 2003. Air China was the only Asian customer for the A318, but decided it had to change to A319s due to engine delivery problems on the A318.

The others

For those existing airlines not part of CAAC’s consolidation plan — and not planning to form an alliance with one of the Big Three — the future may be bleak. The other airlines are largely small, regional operations that have only ever known a CAAC–controlled aviation regime.

For example, China Sky Aviation Enterprises — the only real attempt to form an independent alliance against the Big Three — now looks doomed. This informal (non equity–based) alliance included CPA, Shandong, Sichuan, Shanghai, Shenzen and Wuhan Airlines, and was a brave attempt by mid–level Chinese airlines to fight back against the Big Three. However, with CPA and Sichuan now picked off by China Southern and Wuhan by China Eastern, most observers believe the alliance will fall apart, and that the others will align with one of the Big Three. Shanghai and Shandong, with 23 aircraft each, have the best chance of remaining independent, although in July there were reports in the Chinese press — denied by the parties concerned — that China Eastern was interested in acquiring Shanghai.

Outside this alliance — and firmly in fourth place among China’s airlines — is listed carrier Hainan Airlines, which operates a fleet of 43 aircraft. After securing CAAC approval for international services in 1999, the airline has been keen to reduce its dependence on the domestic market via launching routes to Asian destinations, starting with South Korea. Hainan — which counts among its shareholders the US financier George Soros — has also applied for permission to become the fourth designated Chinese airline to operate to–from the US. Closer to home, Hainan has been leasing 737–700/800s from Boullioun and appears the most aggressive of all the airlines outside the Big Three — for example, in 2001 Hainan became the first Chinese airline to hire foreign pilots.

Finally, although Hong–Kong airlines are not covered in this article, it is interesting to note that in August Cathay Pacific applied to resume flights to the Chinese mainland, for the first time since 1990. Flights ceased then because at that time Cathay bought into Hong–Kong based Dragonair, and under a "one airline, one route" policy it was forced to withdraw in favour of Dragonair. Cathayand its parent Swire still hold a stake in Dragonair but, reportedly, that hasn’t stopped Dragonair from protesting at Cathay’s application. It’s likely that the Big Three are cheering on Dragonair behind the scenes.

As to the future, although consolidation will take time — and there may yet be some upsets to the CAAC’s master–plan — there is little doubt that the Big Three are being given unprecedented advantages in China’s domestic market. Whether they will fully exploit their position remains to be seen, particularly when real market forces hit Chinese aviation. Non–Chinese airlines are keen to increase routes into the country, and new, aggressive start–ups — unburdened by the large overheads and historical/political baggage of the Big Three — are sure to spring up in China. But, whatever happens, the Chinese airline industry of the future will look very different to what it does today.

| 737- | 737- | 737 | 747- | 747- | 757/ | A300/ | A320 | ||||||||||

| 2/300 | 4/500 | NG | 2/300 | 400 | 767 | 777 | 310 | fam | A330/340 | MD11 | MD80 | MD90 | Rus | Chin | Other | Total | |

| Air China | 19 | 10 (7) | 4 | 12 | 10 | 10 | (8) | 3 | 4 | 72 (15) | |||||||

| Air Great Wall | 3 | 3 | |||||||||||||||

| Air Hong Kong | 1 | 1 | 2 | ||||||||||||||

| Air Macau | 9 (6) | 9 (6) | |||||||||||||||

| Beiya AL | 3 | 3 | |||||||||||||||

| Cathay Pacific | 5 | 24 | 12 (3) | 35 (6) | 76 (9) | ||||||||||||

| Changan AL | 3 | 3 | |||||||||||||||

| China Cargo AL | 3 | 3 | |||||||||||||||

| China Eastern AL | 6 | 1 (4) | 10 | 30 (22) | 5 (5) | 3 | 3 | 9 | 67 (31) | ||||||||

| China Eastern AL Wuhan | 6 | 2 | 1 | 9 | |||||||||||||

| China Flying Dragon AV | 8 | 4 | 12 | ||||||||||||||

| China Northern AL | 6 | 3 (7) | 16 | 10 | 35 (7) | ||||||||||||

| China Northern Swan AL | 4 | 3 | 7 | ||||||||||||||

| China Northwest AL | 6 | 13 | 10 | 29 | |||||||||||||

| China Postal AL | 5 | 5 | |||||||||||||||

| China Southern AL | 25 | 11 | (20) | 1 (1) | 18 | 9 | 20 | 84 (21) | |||||||||

| China Southwest AL | 14 | 9 (2) | 13 | 3 | 39 (2) | ||||||||||||

| China United AL | 4 | 30 | 34 | ||||||||||||||

| China Xinhua AL | 6 | 3 | 9 | ||||||||||||||

| China Xinjiang AL | 2 | 4 | 9 | 3 | 5 | 23 | |||||||||||

| Dragonair | 2 | 12 (5) | 8 (1) | 22 (6) | |||||||||||||

| Guizhou AL | 1 | 1 | |||||||||||||||

| Hainan AL | 5 | 7 | 12 | 19 | 43 | ||||||||||||

| Shandong AL | 9 | 14 | 23 | ||||||||||||||

| Shanghai AL | 9 (8) | 11 | 3 | 23 (8) | |||||||||||||

| Shantou AL | 2 | 2 | |||||||||||||||

| Shenzhen AL | 6 | 10 | 16 | ||||||||||||||

| Sichuan AL | 7 | 5 | 12 | ||||||||||||||

| Xiamen AL | 6 | 6 | 6 | 7 | 25 | ||||||||||||

| Yunnan AL | 13 | 4 | 3 | 4 (2) | 24 (2) | ||||||||||||

| Zhejiang AL | 8 | 8 | |||||||||||||||

| Total | 126 | 27 | 67 (41) | 12 | 37 (1) | 71 | 31 (3) | 23 | 102 (48) | 54 (12) | 6 | 29 | 22 | 33 | 15 | 71 (2) | 726 (107) |