Northwest: Asian resurgence behind profit recovery

October 2000

AMR’s interest in Northwest Airlines this past summer drew much attention to the fourth largest US carrier’s formidable array of strategic assets — an extensive Pacific network, a lucrative transatlantic alliance with KLM, strong domestic hubs and a controlling stake in Continental. But Northwest has still not returned to the profitability levels achieved before its 1998 labour troubles. What strategies will it employ to make the most of those assets?

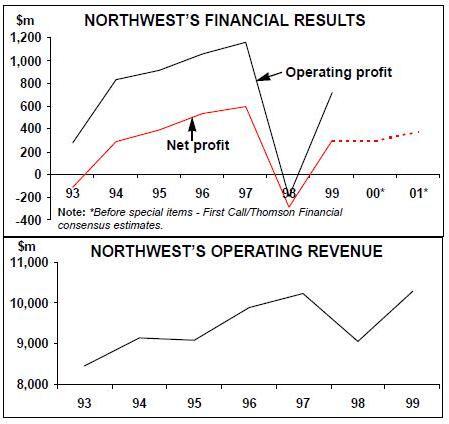

The $300m net profit reported for 1999 was well below the $597m posted on similar revenues for 1997.The latest results, an operating profit of $252m and a net profit of $115m for the June quarter, represent 8.6% and 3.9% of revenues. Those margins are perfectly acceptable at a time when fuel prices are at a record high, but competitors like Continental, United, Delta and American still achieved operating margins of over 10%.

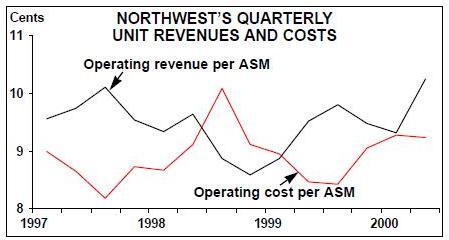

Since the strike Northwest’s unit revenues have rebounded strongly, reflecting a swift and complete recovery of leisure traffic and continued improvements in Pacific markets. Non–fuel costs have remained under control despite expensive new labour agreements and the need to spend on restoring image. In the June quarter Northwest’s costs per ASM excluding fuel rose by just 0.4%.

But the important high–yield traffic segment has still not recovered fully from the 1998 events. Debacles like the January 1999 snowstorm in Detroit, when passengers were forced to remain on an aircraft on the ground for eight hours, have not helped. Even though surveys suggest that Northwest’s customer service and operational performance are now excellent, there have evidently been lingering problems with customer relations.

Over the past year or so Northwest has come at or near the top in the DoT’s domestic on–time performance, flight completion and baggage delivery rankings. This should help it recapture fully its former business traffic share and restore its yield and profit margins (to the extent permitted by fuel prices) in the remainder of this year and in 2001.

Northwest is expected to report essentially flat earnings for the quarter ended September 30, which would be in line with the industry trend. Strong revenue performance, helped by United’s troubles, was offset by higher fuel prices — the carrier bore the full brunt as it was completely unhedged in the latest quarter. But the fourth quarter may see a profit improvement because Northwest has 75% of its fuel requirements for that period hedged at around $19 a barrel.

The current First Call/Thomson Financial consensus forecast for 2000 is net earnings before special items of $3.26 per share. This would be exactly the same as last year’s reported figure or 12.8% higher than the $2.89 reported before special items. The range of 11 analysts’ estimates, from $2.70 to $3.62, is rather wide.

Longer–term earnings outlook is relatively bright in light of the fuel hedges that will kick in, expected full recovery of business traffic and continued strengthening of Pacific demand and unit revenues. The current consensus estimate for 2001 is $4.10 per share or around $377m — still well below the 1996 and 1997 peaks.

Northwest’s cash reserves, which halved to $480m in the six months to December 31, 1998, have now recovered to their former strength — $1.1bn at the end of June. Total liquidity was $2.4bn. However, long term debt has risen from $2.8bn at the end of 1997 to around $3.7bn at present, and stockholders’ equity was just $122m at the end of June.

The favourable financial trends have had little impact on the company’s share price, which fell to a low of $16 in March, after plummeting from $65 to around $25 in the six months leading up to the strike. Speculation about a merger with American temporarily lifted the stock to $39 in early July, but since then the price has fallen back to the mid/high 20s. With a P/E ratio of just 7.6 in late September, the stock continues to be recommended as a “buy” or “strong buy” by most analysts.

Rising labour costs

In the mid–1990s Northwest benefited from an $886m three–year package of wage concessions secured from all of its unions in August 1993. In the second half of 1996 the wages snapped back to the pre–concession levels. The net impact of that on the profit and loss account was not that detrimental (because the company was able to stop issuing stock to employees), but the subsequent inability to secure new contracts led to labour actions and a strike in 1998 that cost the company far more than what it saved in 1994–96.

The strike was settled when the pilots signed a four–year contract, which represented a straightforward compromise — among other things, 3% annual pay rises in return for some productivity concessions. This made possible a new phase in management- pilot relations and subsequent matters, such as pay rates on the A319, were settled quickly.

Since then Northwest has concluded new contracts with seven other unions. The latest of those, a five–year agreement ratified by the flight attendants in May, was particularly welcome because it brought to a close a painful three–year negotiating process. Last year flight attendants rejected an earlier tentative deal and staged a “sickout”, which led to the company filing a lawsuit against the union (dropped when the contract was signed).

Just one more contract needs to be secured to complete the “1996 round” — with Aircraft Mechanics Fraternal Association (AMFA), which represents 9,400 mechanics, cleaners and custodians who voted to get out of IAM two years ago. But those talks appear to be just as tough going as the previous ones. While non–economic issues have been resolved, the two sides reportedly remain far apart on the issue of compensation.

Northwest estimated in a recent SEC filing that the new flight attendant contract will cost it $75m in 2000. The deal provides for retroactive pay from August 1996 at 3.5% of annual salaries and will bring pay rates to industry–leading levels. In combination, the new contracts mean substantial annual increases in labour costs. However, this should not lead to much of a competitive disadvantage because many other major carriers in the US now face similar cost pressures.

. If the AMFA deal is concluded this year, as was earlier hoped, Northwest will have a two–year breathing space before the pilots’ contract becomes amendable in September 2002. The fact that the new contracts are staged will make the next negotiating round easier to manage.

Asian recovery

Northwest has the highest Asian revenue exposure among the US carriers. Its transpacific and intra–Asian services accounted for 23% of its total revenues last year (down from 30% in the mid–1990s), compared to 15% for United, the number two US carrier in that region. Consequently, the Asian crisis had a devastating financial impact. After earning $94–97m annual operating profits in Asia in 1995 and 1996, Northwest posted a small $10.5m loss in 1997 and a massive $465.7m loss in 1998. The 1998 Asian loss far exceeded the combined $336.4m operating profit earned in domestic and Atlantic operations.

The carrier contained the crisis by suspending the worst performing routes, cutting capacity and restructuring its network extensively in favour of more nonstop service in business–oriented markets. This and the start of a gradual recovery in Asia (though not in Japan) about 18 months ago helped reduce the Asian operating loss to $135.1m in 1999.

The slump in Japan bottomed out about a year ago. Northwest’s Pacific division has been recording RPM growth and yield improvements since the third quarter of 1999. In the past three quarters, revenue growth has been running at around 20% and unit revenue growth at 13–19%. The June quarter saw a record 83.1% average load factor in the Pacific division (up 3.1 points). The carrier said recently that while leisure traffic to and from Japan has recovered well, business traffic has been slow to return.

All of this indicates that Northwest is approaching break–even and may even return to marginal profitability in Asia this year. It is well–positioned to capitalise on the region’s recovery and new opportunities.

Two new market developments are worthy of note. First, Northwest is expanding aggressively on promising new business routes like Detroit–Nagoya, which was introduced in 1998 and will see daily 747–400 flights from next April. Second, it has been expanding service in the Detroit–Shanghai market and is bidding for some of the ten new weekly frequencies available to US carriers next year (with obviously no guarantee of getting any — there are seven carriers in the race).

Like many of its competitors, Northwest has been fortunate to experience healthy or improved conditions simultaneously in all of its regions this year. North American traffic and yields have been extremely strong, while the transatlantic market has staged a surprising recovery. After a long decline, Northwest’s unit revenues there rose by 3.5% and 5.3% in the March and June quarters respectively, and passenger revenue surged by 24% in the latest period.

Benefits from freight

Northwest is the only US passenger airline to operate 747 freighters — there are now ten in service after the addition of two last year. Freight has been a strong growth area this year, recording a 25% surge in revenues in the June quarter to account for 7.2% of total revenues.

The reason is the recovery of Asian economies. Northwest’s freighter operations cover Tokyo, Osaka, Hong Kong, Shanghai, Taipei, Bangkok, Singapore, Guam and Manila, while the domestic points served are New York, Chicago, Los Angeles, San Francisco, Seattle and Anchorage. The China freighter service, linking Detroit and Shanghai and complementing the passenger service, was introduced in October 1999.

The latest developments include the launch of the Northwest/JAL cargo code–sharing alliance last month (September), initially on the US–Japan routes. Also, Northwest has just acquired two more “late–model”, ex–United 747–200s, which it is converting from passenger configuration to freighters and expects to place into service in the first half of next year.

Further hub strengthening

Northwest’s hubs — Detroit, Minneapolis and Memphis in the US, Narita in Japan and Amsterdam in Europe — are among its great–est assets and continue to be the focus of expansion and improvement efforts.

Most significantly, Detroit, where Northwest has been growth–constrained for a number of years, will get a new terminal in late 2001 (apparently on time and on budget). The new facility will raise the number of gates from 64 to 99 and will be able to handle 14 widebodies and ten international flights at the same time. The addition of a fourth runway in 2002 will further enhance Detroit’s value as a domestic hub.

The other major building project at present is Satellite 3 at Tokyo Narita, where Northwest will move when it is completed (hopefully) in late 2004 or early 2005. The “absolute state of the art facility” has been designed to facilitate Northwest’s hub–type operation, which is unique among the foreign operators serving Tokyo.

In June Northwest undertook what it called its largest–ever single service expansion when it launched a fourth bank of flights to fill a late afternoon void at its smallest hub, Memphis. Together with its commuter affiliate Northwest Airlink, the carrier added 47 new flights, representing a 25% increase, mostly to cities already served throughout southern US.

Northwest was able to score valuable points in another of summer characterised by flight delays when FAA statistics for 21 major hub airports showed that Minneapolis, Detroit and Memphis were among the best on–time performers in the June quarter.

Predatory complaints

Northwest was previously lucky in that its route system had minimal exposure to low cost new entrants. That changed when carriers like Spirit, Sun Country, AccessAir and Pro Air discovered Minneapolis and Detroit. But none of that has posed any threat because of the extent that Northwest dominates its hubs. AccessAir filed for bankruptcy protection in November 1999, while Pro Air has struggled financially and has just been grounded by the FAA for safety violations.

But Northwest now faces a lawsuit filed by Spirit alleging anti–competitive behaviour, partly due to gate dominance, at Detroit. This is a serious matter that dampens Northwest’s otherwise bright prospects.

To make things worse, Minneapolisbased Sun Country has just released a study, prepared by airline competition expert Dr. Paul Stephen Dempsey, that outlines “the history of predatory and monopolistic practices of Northwest Airlines that have driven low–fare carriers from the marketplace and resulted in higher fares”. The carrier has called for action from Twin Cities’ business leaders and the government.

Fleet plans

Northwest is in the process of gradually simplifying and modernising its fleet, which will include the retirement of its 727s, DC- 10–40s and, eventually, the DC–9s (the MD- 80s have already been eliminated). The carrier continues to take delivery of regional jets, A319s and 757s for expansion. Previously the intention was to retire the 727–200s in 2002 and 2003 (before their age check), but the process will now start in mid- 2001 following a July agreement with Boeing to accelerate deliveries of five 757–200s from 2004 to 2001 and five A320/319s from 2002 to 2001. This will lead to substantial operating cost savings, given the continued escalation of fuel prices.

The A319, which was introduced last year, is also considered to be a good replacement for the DC–9–50. At the other extreme, RJs are also expected to replace some of the DC–9s. Northwest recently took delivery of the last three of 36 ordered AVRO RJ85s and the first of three CRJ–200s due to arrive this year.

This strategy means that the current 171- strong DC–9 fleet may have shrunk to 100- 125 by the time those aircraft will have to be retired, which will be when they start nearing the end of their certified life of 105,000 cycles. But Northwest will still need a replacement 100–seater.

The 747s are utilised mainly on the Pacific, though some fly transatlantic sectors between Pacific runs. The long–term plan is to transfer the transatlantic DC–10–30s to the domestic market, and Northwest is currently evaluating possible replacements.

Alliance considerations

One of Northwest’s greatest strengths is its longstanding relationship with KLM. It was the first to secure antitrust immunity in the US and it is much more advanced in terms of the extent and depth of coordination than any of the other international alliances.

However, efforts to expand the Wings alliance have not been very successful, which has raised questions about where the Northwest/KLM partnership is really heading. The setbacks include the recent breakup of the KLM/Alitalia relationship, after the three–airline combine had already secured antitrust immunity in the US. What will now happen to Northwest’s highly profitable code–shares with Alitalia?

Northwest has continued to expand code–sharing with Continental, in which it holds a 13.5% stake and 50% voting interest. The carrier says that the alliance generated $30m in additional benefits in the June quarter. But Continental now wants to buy back the stake, and the DoJ lawsuit challenging the 1998 purchase is expected to go to court sometime over the next 12 months.

Northwest’s president and CEO John Dasburg provided some interesting insights into the company’s strategy and the workings of the Northwest/KLM relationship at a Merrill Lynch conference held in June. Dasburg explained that the two carriers linked up originally because they both found themselves similarly disadvantaged by their medium size and then divided the responsibility of “finding a solution” in their own regions.

KLM will have the final say about Northwest’s code–shares with Alitalia because “KLM has the final say in Europe and we have the final say in North America”. Dasburg said that KLM would obviously take into account the fact that the healthy profits from the deal go into the joint venture and “will tell us what they’d like us to do with that” before the initial one–year deal comes up for renewal.

The Northwest/KLM agreement has ten more years to run and the airlines are “totally integrated”, so Dasburg believes that the alliance will survive any new relationships that the two develop in their respective regions.

Did Northwest ever seriously consider AMR’s proposals? It reportedly turned down American’s final offer of up to $65 a share as inadequate, demanding at least $100 per share. Dasburg pointed out that while the company is by law obligated to consider attractive offers, embarking on a right strategy (a reference to the KLM alliance) is another way to maximise shareholder value.

Northwest is anxiously waiting for the DoJ’s response to the proposed UAL/US Airways merger, because it is a much more integrated transaction than the blocking rights Northwest secured in Continental. If the UAL/US Airways deal is allowed, Northwest believes that the DoJ will withdraw its objection to Northwest/Continental and the two could then apply for and obtain antitrust immunity. Otherwise, Northwest is prepared to defend its strategy in court.

| In operation | On order | |

| 727-200 | 31 | |

| 757-200 | 48 | 25 |

| 747-200 | 23 | |

| 747-200F | 10 | |

| 747-400 | 14 | |

| A319 | 16 | 53 |

| A320 | 70 | 12 |

| A330 | 16 | |

| DC-9 | 171 | |

| MD-80 | 8 | |

| DC-10 | 45 | |

| Total | 436 | 106 |