India's LCCs struggle through tough times

May 2014

India’s LCCs have toiled for years to survive and scrape a profit in a market with one of the highest passenger growth rates in the world. But that same growth rate and the opening up of the aviation market to foreign investment is now encouraging yet another wave of new airlines in India. Can the established Indian LCCs survive?

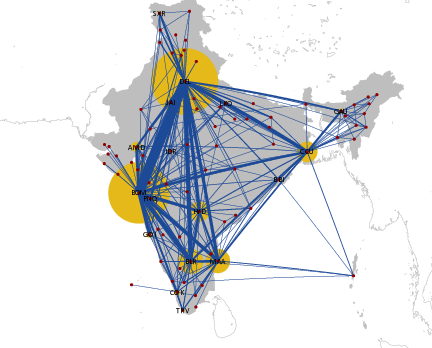

As can be seen in the graphs on this page, both domestic and international traffic has already risen significantly in the last decade, and according to Boeing over the next 20 years India is forecast to have one of the highest passenger traffic growth rates in the world, driven by GDP growth and higher disposable incomes, particularly among the growing urban-based middle classes, who number around 300m-400m out of a total population of 1.3bn.

The Indian government began to liberalise significantly the aviation industry in 2004 (see Aviation Strategy, December 2003 and June 2007), and a number of LCCs have sprung up since then to exploit this liberalisation. However, in September 2012 the government took the major step of allowing foreign airlines to own up to 49% of local carriers, and as a result overseas carriers began hunting for opportunities to enter the Indian market. Etihad Airways moved first by paying $380m for 24% of Jet Airways in 2013, while both Singapore Airlines and AirAsia are setting up Indian operations in the near future. Add in purely Indian start-ups such as Air Costa and Air Pegasus, and the prospects for the Indian aviation industry look bright, particularly given that the Indian market is still hugely underserved, with hundreds of large towns and cities that have little or no air connection.

But while prospects for Indian aviation may well be bright as a whole, for the incumbent LCCs the impact of this new wave of competition could be fatal. Many of them have struggled to convert the growing willingness of the middle classes to travel by air into a profitable business model, because although this market is large and growing, it is still relatively “poor” by western standards of income, and as a result is very sensitive to fare prices. This high elasticity of demand has encouraged LCCs to cut fares at every opportunity in order to boost demand, but when all airlines do it the result is a downward spiral in overall revenue and profitability. And that spiral is continuing — a latest round of air fare cuts initiated by SpiceJet in April 2014 has encouraged fares to fall to their lowest levels in around two years.

Note: The thickness of the lines represent the volume of capacity on each route. The area of thelarge circles relate to total domes c capacity at the top airports.

The market is also distorted by high airport charges and taxes on jet fuel and — perhaps most significantly of all — by the competition provided by Air India, which continues to be supported by the Indian state after making colossal losses. To make matters worse, over the last year India’s airlines have struggled to overcome the impact of the rupee’s sharp depreciation against the US Dollar (by around 11% in just 12 months), which has — along with significantly higher fuel prices — helped to increase operating costs for Indian airlines by at least 20% in 2013.

| Fleet (orders) | IndiGo | SpiceJet | GoAir | Air India Express | JetKonnect |

| A320 | 78 (7) | 18 | |||

| A320neo | (160) | (74) | |||

| A321neo | (20) | ||||

| 737-700 | 5 | ||||

| 737-800 | 37 (17) | 17 | 4 | ||

| 737-900 | 2 | ||||

| 737-900ER | 6 | ||||

| 737MAX | (42) | ||||

| Dash 8 Q400 | 15 (15) | ||||

| ATR 72 | 5 | ||||

| Total | 78 (187) | 58 (74) | 18 (74) | 17 | 16 |

In the following pages Aviation Strategy takes a look at each of the major Indian LCCs in turn.

Indigo

Based at Gurgaon, IndiGo was launched in 2006 by Rahul Batia, owner of Indian conglomerate InterGlobe Enterprises, and Rakesh Gangwal, a former CEO of US Airways who now runs US-based Caelum Investments. Those two entities hold 51.1% and 48% stakes respectively in the airline. ~

Today IndiGo has the largest fleet of all the Indian LCCs, with its 78 A320s having an average age of less than three years. With its main base at Delhi and with secondary bases at Mumbai and Kolkata, IndiGo operates to 31 domestic and five international destinations; it started international operations in 2011 and currently operates from Mumbai and Delhi to Bangkok, Dubai, Kathmandu, Muscat and Singapore.

The airline has a hefty 187 aircraft on order (the largest order book of any Indian LCC), comprising 167 A320s and 20 A321s, the majority of which are neo models. IndiGo placed an order for 180 Airbus aircraft in 2011, worth $15bn at list prices, and 160 A320neos will start arriving from 2016 and 20 A321neos will be delivered from the following year, with all the neo being delivered by 2025.

IndiGo is likely to add substantial new orders sometime this year (for as many as 250 aircraft, one analyst believes) and it would be a shock if they were for anything other than further A320neos — although the airline has previously indicated that it may look at regional aircraft at some point in the future if market economics make sense.

IndiGo tightly follows a traditional LCC model, with single aircraft type and a single class product that has paid-for meals and no in-flight entertainment. Perhaps because of that focus it has a 30% leading share of the Indian domestic market — and unlike many of its rivals IndiGo is profitable.

Some analysts have speculated that IndiGo makes a substantial book profit by selling and leasing back its aircraft, but the airline has denied this, and it’s difficult to verify either way given that as an unlisted company IndiGo releases relatively few financial details.

IndiGo has yet to post results for the financial year ending March 2014 (they are likely to be revealed around September, as is customary among almost all Indian airlines), but in the 2012/13 financial year it reported a substantial six fold rise in net profit to Rs7.9bn (US$143m), its fifth straight year of profitability. The increase was based on a 39% rise in capacity and 20% rise in average yield over the year, with revenue up 65% year-on-year to Rs95bn (S1.7bn). Operating profit for the 2012/13 financial year totalled Rs9.9bn ($181m).

Aditya Ghosh, president at IndiGo, says the secret to its profitability is a relentless pursuit of cost cutting and a focus on a basic and simple product. “We haven't tried anything fancy, or bizarrely different,'' he says, and the airline’s reputation for reliability and consistent products allows it leeway to charge higher fares than many of its LCC competitors — and even more than full-service competitors Air India and Jet Airways on certain routes. But not too high — Rahul Bhatia, group MD of InterGlobe Enterprises, which owns IndiGo, says that as with all Indian airlines “the weak rupee and high fuel prices are putting pressure on margins”, but that “the religion in IndiGo is to keep prices low, otherwise I don't think we can grow at 20-30% annually”.

The longer-term plan is to keep growing by around 10-15 aircraft a year for the next decade, which appears sustainable, and a potential IPO in 2015 or 2016 is a distinct possibility. IndiGo took a long look at doing an IPO back in 2010 after hiring no less than five financial advisors, but decided to not go ahead at that point. However, prior to an IPO it‘s possible that the airline may attract a foreign investor; Qatar Airways is apparently interested in acquiring a stake. The two airlines know each other well — in May 2013 Qatar and IndiGo apparently held talks about a codeshare deal, though this came to nothing.

A financial tie-up would make strategic sense for both carriers. The Middle East has proved an attractive market for IndiGo — it operates more than 20 flights week between India and the Gulf regions, with its routes to Dubai and Muscat proving popular with the Indian expat and working community in the region.

Qatar may be looking to match rival Etihad’s purchase of a stake in Jet Airways, though the Doha-based carrier has also been linked with an investment in SpiceJet, as well as reportedly looking for codeshares with virtually the entire Indian aviation including Go Air, IndiGo, SpiceJet and even Air India.

SpiceJet

Based at Chennai airport, SpiceJet’s origins date back to early 1990s when ModiLuft was launched by entrepreneur S K Modi in partnership with Lufthansa to become one of the first full-service carriers to emerge to provide competition to Air India. ModiLuft ceased operations in 1996 but its AOC was taken over by Royal Airways. The owners of Royal, by this time a dormant airline, made the bold move of planning and setting up India’s first LCC and ordering new 737-800s. The Mumbai and Delhi investor presentations not only raised the necessary capital but accidently helped launch two other rival LCCs. In 2010 a 37.7% share of SpiceJet was acquired by Indian conglomerate the Sun Group, which is controlled by billionaire Kalanithi Maran, and this has since risen to at least 49% (with the rest on a free float).

SpiceJet’s first LCC operations began in 2005 and today SpiceJet operates a fleet of 58, with an average age of 4.5 years, to around 41 domestic and seven international destinations. In December last year SpiceJet signed a three-year interline agreement with Singaporean LCC Tigerair, becoming the first Indian LCC to agree such co-operation with a foreign airline.

SpiceJet has 74 aircraft on firm order, comprising 17 737-800s, 42 737MAXs and 15 Dash 8 Q400s. The 737 MAX 8 order was announced this March (though it was reportedly agreed between Boeing and the airline last October), in a deal worth $4.4bn at list prices, and with the first aircraft due to be delivered in 2018. The MAX order has apparently taken the place of the outstanding 737-800 firm order, though for the moment the -800s still remain in the Boeing order book.

The 15 Q400s in SpiceJet’s fleet connect SpiceJet’s main bases to secondary and tertiary cities in India, and another 15 of the type will expand this network.

SpiceJet is the second-largest LCC in India with an approximate 20% share of the domestic market, but despite that and even with the deep pockets of its owners, SpiceJet has struggled to make a profit.

In the first three-quarters of the 2013/14 financial year (the nine months to 31st December 2013), SpiceJet saw revenue rise by 12.6% to Rs47.7bn ($772m), although the operating result turned from a profit in the first nine months of 2012/13 to a Rs5.9bn ($96m) operating loss in April to December 2013. The net result similarly plunged from a Rs5.4bn ($97m) loss to a Rs6.8bn ($110m) loss over the same comparative nine-month period.

The airline blames the weaker rupee, which inflated lease and fuel costs by around Rs630m ($10m) in the last three months of 2013. It adds that fuel prices were 9% higher in the same quarter year-on-year, with fuel costs accounting for 52% of revenue in the October-December 2013 period, compared with 45% a year previously.

Overall costs per ASK rose 10% in the quarter, which was not offset by a 3% rise in passenger yield in the same period. SpiceJet adds that “demand for air travel softened during the year, exacerbated by more seats due to planned additional aircraft by the Indian aviation industry — including SpiceJet”. Load factor fell significantly in the three month period to December 2013, from 75% to 70.5%, and overall revenue per ASK fell 6% in the quarter.

SpiceJet is attempting to return to profitability through a series of measures that include cost reductions, productivity improvements and “a complete network and schedule redesign”. This includes a greater emphasis on attract higher margin passengers. While an LCC, the airline has been straying into full-service enhancements. SpiceJet offers premium seats, with priority check-in and extra baggage allowance, and the airline is reconfiguring its 737 aircraft to offer five seat rows with enhanced legroom. SpiceJet also recently launched an FFP for business travellers called Corporate Frequent Flyer, where customers booking through corporate accounts gain one free flight for every six tickets booked. And this May SpiceJet also launched its biggest advertising campaign for more than three years, which reportedly will include television adverts in the coming months.

Some analysts believe that though laudable, these efforts will not succeed in make the airline profitable, and that the real problem is that SpiceJet is significantly undercapitalised, with an urgent need to attract new investors and capital. Indeed the airline is expected to post a loss of as much as Rs10bn ($162m) for the full 2013/14 financial year, which would be not far off its accumulated losses over the previous seven years.

The intentions of SpiceJet’s current owners are unknown, but the carrier will reportedly get a new CEO this summer when Sanjiv Kapoor is promoted from his current position of COO (which he became in November 2013). The previous incumbent CEO was Neil Mills, who left last year to join Philippine Airlines. An American citizen, Kapoor was previously CEO of Bangladesh’s GMG Airlines.

The first item in his in-tray will be whether to continue with deep fare cutting. SpiceJet initiated another round of fare wars in India earlier this year, which was inevitably copied by its competitors even though one of them called SpiceJet’s move “suicidal”.

GoAir

GoAir was founded in November 2005 by Jehangir Wadia, a member of the family that run the Wadia group, an Indian conglomerate that dates back to the 18th century and which today has interests in everything from chemicals to health care.

With Jehangir Wadia as CEO, the airline has grown slowly, though the company says that this has been intentional as it prioritises profitability ahead of winning market share. GoAir currently operates a fleet of 18 A320s (with less than four years’ average age) to more than 20 destinations in India. It offers a partly traditional LCC model, with a single model fleet and paid-for meals, although it also offers a premium service called GoBusiness that includes meals, a spare middle seat in between passengers on selected routes (such as Mumbai-Delhi). It also offers an FFP called Go Club, which was the first FFP to be offered by an Indian LCC.

GoAir has 74 A320neos on order, of which 72 were placed in 2011 in a deal worth S5.4bn at list prices. Deliveries are due to begin in 2016, with aircraft arriving at around 15 per year after that. Until then growth will come by further leased aircraft, according to CEO Giorgio De Roni, (who has been in the position since 2011 and who was previously chief revenue officer of Italian carrier Air One) with two more aircraft being added by the end of this year and further leased aircraft in 2015.

GoAir’s main operation is based at Mumbai, with a secondary base at Delhi, and flights to and from Delhi and Mumbai account for approximately half of all services, with the Mumbai-Delhi trunk route by far its most important route.

GoAir has an approximate 8% to 9% share of the Indian domestic market, and it particularly gained share after the exit of Kingfisher Airlines in 2012. In the 2012/13 financial year (ending March 31st) it made a Rs1bn ($19m) net profit, compared with a Rs1.3bn ($26m) loss in 2011/12 — although all of the profit came from the sale and leaseback of aircraft; excluding sale and leasebacks, GoAir’s losses would have been Rs793m ($14m).

However, in the first six months of the 2013/14 financial year (April-September 2013) GoAir saw passengers carried rise more than 30%, to 2.6m, and the airline says it’s on target to record another profit in the 2013/14 financial year.

GoAir’s fleet will reach around 37 aircraft by the end of 2017 and it is keen to launch international services, although as a result of its current size GoAir is prohibited from operating these under government regulations called the 5/20 rules, whereby domestic airlines are not allowed to operate internationally unless they complete five years of domestic operations and have a minimum fleet of 20 aircraft.

The airline has lobbied unsuccessfully to overcome these restrictions, although some analysts believed they may finally be scrapped by the government this summer — which will be irrelevant to GoAir as its 20th aircraft should be delivered in July or August anyway, which will then fulfil the last of these criteria.

Either way, GoAir will start international operations by the end of this year at the latest, with at least 10% of its capacity being dedicated to international services — though this will depend on securing traffic rights into the markets it targets. These are believed to be in the Gulf region and neighbouring south-east Asia countries, with GoAir likely to prioritise international services from second tier cities — i.e. not from Mumbai and Delhi, where international competition is fierce.

Domestically, growth will also be seen primarily on routes to secondary cities, such as Patna, Lucknow, Jaipur, Kochi, Chandigarh, and Jammu and Kashmir, with De Roni saying that “metro to metro business has not witnessed a similar pace of growth”. A number of other secondary cities will be added over the next two years, and in particular in the east of the country, which the airline believes is particular underserved.

Along with SpiceJet, GoAir is also mentioned by analysts as being potentially available for foreign investment, and the Indian press has reported that talks have been held with Lufthansa, Emirates and Qatar Airways. Last year De Roni said that: “The shareholders are not interested in selling the company, but they want a partner to support the growth of the company”. JP Morgan has been appointed to help with the search for a “partner”, and sources suggest that negotiations are advanced with at least one carrier.

Air India Express

Air India established its LCC subsidiary — Air India Express — in 2005 to operate to destinations within a four hour flying time from the country, with a typical LCC turnaround of no more than one hour at all airports.

Air India Express operates a fleet of 17 737-800s (four others were recently returned to lessors), with an average age of more than six years. The carrier is headquartered at Cochin airport in and has two other main operating bases — Calicut airport in Kozhikode and Trivandrum airport in Thiruvananthapuram. As such most of its flights operate to and from the south of the country, with 12 domestic and 13 international destinations served.

The majority of Air India Express’s international focus is on routes to the Middle East — including to Dubai, Sharjah, Abu Dhabi, Al Ain, Muscat, Salalah, Bahrain, Doha and Kuwait — where the carrier serves Indian expat communities in those countries. The remaining international destinations are Singapore, Kuala Lumpur, Columbo and Dhaka.

However, under a new CEO appointed in April this year — K. Shyam Sundar — Air India Express has plans to significantly increase its international network outside of the Middle East as part of an expansion that will see the fleet rise to 36 by 2017. 19 more 737-800s will be leased over the next three years, and it has already released a tender for the dry lease of eight aircraft. However, the process of acquiring new aircraft is somewhat complicated for Air India Express as it needs to get government permission for major new expenses, which given the precarious financial position of Air India is not an easy process.

Nevertheless, potential new destinations believed to be under analysis include Iran, Russia and other CIS countries — although as yet Air India Express will not confirm those target markets. Sundar and other senior Air India Express executives believe that there is significant demand for LCC services to the Middle East and Asia that is currently going to competitors, and that an expanded Air India express network will win passengers that want to be loyal to the Indian flag carrier.

The airline offers a single class service, although free in-flight meals and entertainment are included with all fares, and passengers can now pre-select seats for a fee. However, last year Air India Express reduced its free baggage allowance from 30kg to 20kg per passenger, charging for any extra weight, which was met with criticism from some passengers.

In terms of financial reporting Air India Express is part (and the only part) of Air India Charters Limited, which in turn is a subsidiary of Air India, and the last full report made available for Air India Charter is for the 2011/12 financial year ending March 31st 2012. Reported revenue for the year was Rs13.8bn ($267m), a 2.2% rise on the previous financial year, with net loss totalling Rs6bn ($116m), compared with a Rs3.9bn loss in 2010/11. The improvement in revenue was due largely to a 2.5% increase in load factor to 71.0% in 2011/12, and a 7.6% rise in yield. During the 12 month period Air India Express carried 2.31m passengers, compared with 2.38m in the previous financial year.

Air India Express now operates independently of its parent airline and is building up its own pilot workforce. Despite having its own AOC in previous years the LCC has faced problems as it used Air India pilots for all its flights, and they were inevitably prioritised to Air India flights, with Air India Express getting pilot hours only when it suited their parent’s schedules. This even led to flights being withdrawn, and two years ago the airline told the Indian aviation ministry that it needed at least 200 more pilots in order to operate effectively.

That shortfall has now been made up, with direct hires to the company and the building up of its own pilot training resources. The extra pilots have also helped increase aircraft utilisation, which according to one report was as low as six hours a day in 2012, well below standard.

JetConnect

Jetconnect (or JetKonnect as variously spelled by the company) is an LCC based in Delhi that has a somewhat complicated history. The carrier was previously known as Jet Airways Konnect and prior to that (until 2012) it was called Jetlite. That airline previously operated as Air Sahara, an Indian carrier that began life under the name Sahara Airlines back in 1993. Sahara was a strong brand in India in its rôle as a micor-lender. Sahara Airlines became Air Sahara in 2000, and in 2007 it was bought by Jet Airways for $340m, after which it was immediately renamed as Jetlite. Finally, in March 2012 Jetlite was submerged into Jet Airways low cost brand JetConnect (which had launched in 2009), then becoming a separate airline under that name.

Parent company Jet Airways was founded (and is still chaired) back in 1993 by Naresh Goyal, one of the richest men in India, and today it operates 114 aircraft domestically and internationally. However it has been loss making for a considerable number of years, although white knight Etihad Airways bought a 24% stake in Jet Airways for around $380m last year (see Aviation Strategy,November 2013).

Most immediately the Gulf carrier’s injection of investment and resources at least makes JetConnect’s parent a more stable entity, but the deal also opens up the question of just how Etihad sees JetConnect fitting into an overall strategy for Jet Airways.

Although flights and schedules at JetConnect have been altered in order to connect better with Jet Airways and Etihad flights, there were reports last year that in anticipation of the Etihad deal Jet Airways may want to convert JetConnect into a full service airline, in order to bring it closer to the Jet Airways product and to avoid so-called “brand confusion” with its parent. That hasn’t happened so far, although just how much JetConnect is an actual LCC is open to debate.

Today the airline operates an assorted mix of 16 aircraft — comprising five 737-700s, four 737-800s, two 737-900s and five ATR 72s — on a solely domestic route network linking 55 destinations. As well as a varied fleet it has other “non-LCC” attributes, such as two classes on selected services, with a Première class offering in-flight meals, improved seat pitch, dedicated check-in counters and lounge access, as well as an FFP called JetPrivilege (effectively exactly the same as Jet Airways’ FFP).

JetConnect has an estimated 6-7% market share of the Indian domestic market, which it maintains through constant fare wars with its rivals — in January this year it slashed fares by 50% via a 30-day advance purchase fares on certain routes (a discount that ran until April).

JetConnect’s results are not separated out from its parent, though in the first three-quarters of the 2013/14 financial year (the nine months ending December 31st 2013) Jet Airways reported a net loss of Rs15bn ($245m), with domestic operations (including both Jet Airways and JetConnect) accounting for Rs52bn ($849m), though this was down 3.9% compared with the April to December period of 2012.