Southwest: tinkering with the tried and tested formula?

January 2004

The US airline industry structure is in the process of changing dramatically, with the rapid rise of LCCs coming at the expense of the legacy carriers. At least, that will be the outcome if the large network airlines do not get their act together and prevent further significant erosion of their market shares.

The LCCs that are spearheading the change — JetBlue, AirTran and others — belong to a new breed of aggressive and profitable carriers. First, they are growing extremely rapidly, not just in short haul but also coast–to coast markets. Second, they have opted out of many traditional Southwest formulas, such as operating a single 150–seat aircraft type and offering a no–frills product.

Third, they have gone a step further by setting new standards for in–flight service.

Many people are now wondering how Southwest, the airline that pioneered the original LCC concept, will fit in with all this. Is it going to stick to the strategies that have worked so well for it for 30–plus years? Or could it, too, now benefit from some changes?

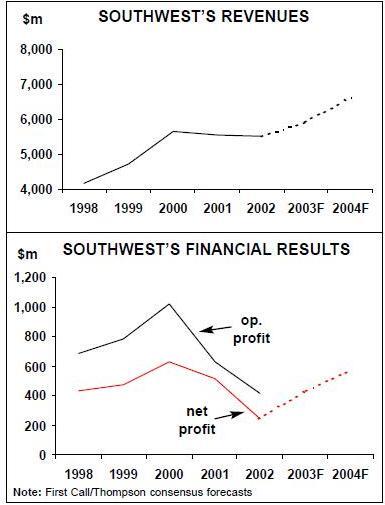

Southwest continues to be one of the industry’s strongest profit performers and hugely successful in the marketplace. It has remained profitable through the industry crisis, albeit at reduced margins. In the latest reported quarter (3Q03), its operating margin had recovered to double digits (11.9%).

The margin gap with the high–cost majors is wider than ever before and is expected to stay that way. By 2005, when the legacy carriers will have returned to, at best, marginal profitability, Southwest’s operating margins are expected to have recovered fully to the 17–18% level seen in 1999 and 2000.

Like other LCCs, Southwest has made significant market share gains during the industry crisis. Although this was probably not the intention, it has gained market share in the past two years simply by the virtue of maintaining pre–September 11 2001 service levels in most markets when competitors cut capacity significantly. According to figures presented by its treasurer Laura Wright, between 1998 and 2003 Southwest’s domestic capacity (ASM) share rose from 7.7% to 11.5%, while other LCCs' share (including America West) increased from 9% to 14.4%.

The legacy carriers' ASM share fell from 83.3% to 74.1%.

However, Southwest’s share price has been rather volatile in recent months, reflecting various investor concerns (as opposed to just excessive valuation — the main reason why LCC stocks plummeted by 40% between mid–October and mid–December).

First, analysts and investors worried that Southwest might never get its growth back to the 10% level. There were fears that the airline — traditionally cautious about entering new markets and, after September 11 2001, determined to remain extremely conservative "until there is more clarity in the earnings picture" -might lose good growth opportunities to JetBlue, AirTran and others if it waited much longer.

Next, after Southwest’s big Philadelphia announcement in late October, there were some jitters about the aggressive nature of that expansion. Why was the airline departing from its usual strategy of flying to cheaper and less congested secondary, non–hub airports? In late November and early December the shares took further hits as investors began to fear that costs were getting out of control.

New guidance from Southwest indicated that its unit costs (CASM) would rise by a hefty 4% in the fourth quarter. This prompted analysts to revise down their 4Q earnings estimates. The jitters about LCCs generally reflect the fact that competition is really heating up on the East Coast. Last year saw the rapid build–up of Delta’s Song. JetBlue and AirTran are both expanding aggressively — most recently, in Boston and Baltimore, respectively.

Edward Beauvais, former head of America West, is working to start a new low–cost airline out of Pittsburgh in June. Atlantic Coast is planning to build a large low–fare hub operation at Washington Dulles from mid–2004.

But what really makes the current situation different is that the legacy carriers are at last beginning to respond aggressively to the LCC threat. This is taking the form of both general capacity addition (aggregate ASMs are up significantly in 2004) and competitive moves in specific markets. As an example of the latter, American is now offering a free round trip ticket anywhere to AAdvantage FFP members who purchase two round trip tickets in selected Northeast–Florida and Northeast- California markets that JetBlue serves — an aggressive move by any standards.

Southwest is doing its bit, first, by accelerating its overall capacity growth significantly this year and in 2005, and second, by adding Philadelphia as its 59th city from May. Philadelphia — the nation’s fourth largest city and US Airways' primary hub — represents an unusually aggressive move for the low–fare carrier, which has traditionally avoided direct confrontation with the majors.

Resumption of rapid growth

Southwest’s CFO Gary Kelly recently described increased competition with LCCs as "potentially a different ball game". What does that mean in terms of strategy? After growing extremely cautiously through the past two years' industry crisis, Southwest is now accelerating ASM growth from 4.2% last year to around 7% in 2004.

Subsequently, in 2005 and 2006, the current aircraft orders and options would facilitate a return to the 10%-plus annual ASM growth seen in the 1990s.

This is happening in large part because Southwest is feeling more confident about economic and industry prospects. However, it is also responding to the growing presence of LCCs. As Kelly explained it in a recent conference call: "There is a higher risk of being pre–empted in some markets. We've never been driven by a concern of being pre–empted, but our decision to step up our near–term growth does reflect that. We sensed some urgency to get there first — at least more than we did in the past."

As a result of some aircraft order additions and delivery accelerations in recent months, Southwest is now scheduled to take a staggering total of 47 new 737–700s in 2004, up from 17 last year. This is in sharp contrast with the other US major airlines' non–existent or meagre deliveries this year. It is also substantially more than what the other (much smaller) LCCs are taking.

The 47 new aircraft represent an all–time annual record for Southwest. The net addition of 30 aircraft (after the retirement of 17 older 737–200s) will be the same as in 2000 and will increase the total fleet to 417 by the end of 2004. Next year’s schedule currently includes 23 firm deliveries, 11 options and five retirements.

Philadelphia: rationale and plans

Philadelphia, due to be added on May 9, will be Southwest’s first new city since late 2001. The plan is to serve a variety of short haul and long haul destinations, based on demand. The six initial markets — ChicagoMidway, Las Vegas, Orlando, Phoenix, Providence and Tampa Bay — will see a total of 13 daily departures.

Philadelphia was a great surprise, particularly since Southwest had also considered secondary airports in the area, including Trenton in New Jersey and Allentown in Pennsylvania, which would have been more in line with its traditional strategy.

But the airline insisted that Philadelphia met its key criteria.

First, it was a classic overpriced and under–served market, with only 5–10% of traffic carried by discount airlines. Second, infrastructure and airport costs were attractive.

Third, there was a rare opportunity to obtain gates.

Southwest had apparently considered Philadelphia for 15 years, but until recently there were no gates available and the airport was too congested to allow efficient operation.

Then four ex–TWA gates became available after AMR purchased TWA, and since September 2001 US Airways has cut its daily flights from 410 to 384. Although Southwest plans to utilise only four gates initially, it could grow to eight, facilitating up to 80 daily flights.

While US Airways' shrinkage played a major part in Southwest’s Philadelphia decision, competitively the move was probably more aimed at JetBlue and AirTran — namely preventing other LCCs from establishing a presence at that airport. According to Southwest executives, the Philadelphia move does not represent any change in strategy.

The airline is only interested in overpriced and under–served airports, whether hubs or secondary airports. The problem with hubs is that they may be overpriced, but generally they are not under–served.

Southwest is counting on stimulating demand with low fares so that total traffic in the Philadelphia markets multiplies. With US Airways currently dominating those markets with unrestricted fares four or five times the fares that will be introduced in May, the famous "Southwest effect" can be taken for granted.

The main risk to Southwest is Philadelphia’s congestion. "In the final analysis we simply concluded that the risk was worth the potential reward", explained CEO Jim Parker at a recent conference. Southwest is such a strong competitor that it probably does not make any difference from its point of view how US Airways responds — except if US Airways pulls out entirely and disposes of its Philadelphia gates and facilities.

Many people have expected Southwest to start a major expansion from St. Louis, after American halved its daily flights there on November 1. But so far Southwest has only announced plans to boost its daily flights from 55 to 57, as it apparently has concerns about airport costs at St. Louis.

A second fleet type?

Dedication to a single aircraft type, the Boeing 737, has been the cornerstone of Southwest’s low–cost strategy — and one that was previously copied by other low–cost entrants. However, JetBlue and AirTran have recently opted for the flexibility offered by two aircraft types. JetBlue has ordered 100–seat EMB–190s for expansion in smaller markets, to supplement its A320 fleet from 2005.

AirTran will start adding 737–700s in June for transcontinental expansion, to supplement its 717 fleet.

Other LCCs on both sides of the Atlantic are also seriously considering adding a second aircraft type. They are tempted by new types of market opportunities that have come about during the industry crisis (often when weaker carriers pulled back or disappeared), as well as the current low aircraft acquisition and ownership costs.

Southwest’s top executives have indicated that although at this point the airline remains dedicated to a single aircraft type and will not reconsider 50–seat or 70–seat regional jets (after firmly rejecting them in the past), it is now taking a serious look at the EMB–190.

In the first place, Southwest is looking at the EMB–190 simply because it is an interesting new addition to the 100–seat category. Its top executives have stressed that they would be extremely hesitant to walk away from the advantages of operating a single aircraft type.

They are "not even close to reaching a decision on that question".

Kelly has made the point that a 100–seat aircraft may not be sufficiently different in size from Southwest’s 137–seat 737s to add much flexibility. Certainly, the benefit of the 100–seat EMB–190 will be greater to JetBlue since its other aircraft are 156–seat A320s. Some people take the view that Southwest already effectively operates two or three different aircraft types — the 737–200, the 737–300 and the 737–700 (the 200s are being phased out).

The key question is: does Southwest want to serve smaller markets? So far it has only been interested in relatively large markets. It is worth noting that JetBlue identified 900 potential markets that could be developed profitably with a 100–seater, compared with 305 markets suitable for the A320.

What about some frills?

The new–generation LCCs are much more up–market than Southwest, with assigned seating, more legroom and latest–technology in–flight entertainment systems. The ability to offer low fares without sacrificing any aspect of service has made JetBlue, in particular, a real hit in the marketplace. The fact that so many LCCs are moving in that direction may even raise travellers' general expectations.

While Southwest is renown for its great service and friendly workers, its very simple product may soon look dated. Consequently, in recent conference calls analysts have quizzed its top executives about possible changes in that area.

Southwest has denied that assigned seating or any other major changes to the model are being considered. However, Kelly disclosed recently that the airline is studying new–technology in–flight entertainment systems.

This is hardly surprising in light of the huge popularity of the in–flight satellite television pioneered by JetBlue and also introduced by Frontier, WestJet and Song. JetBlue and AirTran have also announced plans to introduce digital satellite radio later this year, with JetBlue also adding pay–per–view films.

Southwest is about half–way through a five–year programme, due to be completed by the end of 2005, of introducing a new paint scheme and interiors, including leather seats, on its entire fleet. Otherwise, the airline will continue to count on its great corporate culture and high employee morale to keep the air travel experience fresh and unique for its passengers. CEO Jim Parker said recently that he believed employee morale was at or near an all–time high. He said that his number one focus is maintaining the corporate culture.

That involves keeping in contact with workers on a personal level, which is obviously more difficult now that Southwest is a large company. One solution has been to develop "local leaders" — people at every facility, station, pilot base, etc. that really understand the corporate culture and values and share that with the employees.

Labour cost pressures

Southwest’s number one objective is to maintain its cost leadership. But there are some challenges on that front because of continued labour cost pressure, resulting from five new contracts concluded over the past year or currently under negotiation.

In particular, pilot costs are rising sharply, reflecting a 6.4% wage increase last September and a 13.6% hike in September this year. The pilots took a five–year pay freeze in the 1990s, but the new rates will still make them among the best paid in the industry.

In one analyst’s estimate, the new pilot contract alone will add $60m to costs this year.

However, Southwest is optimistic that it can maintain its CASM at 7.5 cents per ASM in 2004 and 2005. It is seeing some productivity offsets and will continue to aggressively seek cost savings both internally and externally to retain its low cost structure.

One of the most important new measures, implemented last month, was the elimination of travel agents' commissions — a move that is expected to save about $40m annually. Southwest had been the last major airline paying base commissions. As Kelly explained it: "With more low–cost competition looming, it was time to make that change".

Financial outlook

Southwest will be the only US major carrier to report a profit for 2003 (the results are expected on January 22). In early January the First Call consensus estimate was a net profit before special items of 37 cents per share, which would represent a 54% increase over the 24 cents earned in 2002.

Aside from the labour cost pressures, prospects are excellent. The airline remains extremely well hedged for fuel, having covered 83% and 45% of its planned consumption in 2004 and 2005, respectively, with derivative instruments that effectively cap prices at about $23 per barrel. On the revenue side, Southwest’s traffic mix has recovered to a much greater extent than what the other large carriers have experienced.

Analysts expect Southwest’s EPS growth to accelerate and profit margins to recover fully as capacity growth is stepped up. The current consensus forecast for 2004 is a profit of 58 cents per share (up 57%), though individual analysts' estimates range from 52 to 70 cents.

Significantly, Southwest has maintained investment grade credit ratings through the industry crisis. Its balance sheet is stronger than ever, with total assets of $9.7bn, shareholders' equity of $4.9bn and long–term debt of $1.5bn at the end of September. After paying down some debt in October, the company projected its lease–adjusted debt–to–capital ratio to be below 40% at year–end (100%- plus is now typical for the other large majors, and even JetBlue is in the high 60s).

Southwest is therefore well positioned to meet its substantial aircraft capital spending requirements over the next few years. 2004 will see total capital spending peak at $1.8bn (compared to $1.2bn last year and $1.4- 1.5bn in 2005). But there are no pension under–funding issues because the airline only offers a defined pension contribution plan. With $2bn in cash at the end of September, $575m of available credit facilities and healthy cash generation, Southwest is expected to continue to be largely self–financing.

However, it has indicated that it wants to carry a large cash balance for emergencies. Because of that and 2004’s unusually heavy spending needs, the airline expects to raise external funding to the tune of $300–500m this year.