Continental: cashing in on the positives

January 2001

Continental enters 2001 with one unique advantage over its competitors — no union contracts coming up for renewal this year. The company expects to complete a $450m share buyback from Northwest on or soon after January 22, which will give it freedom from the influence of a major shareholder for the first time in eight years. How will Continental cash in on these positives?

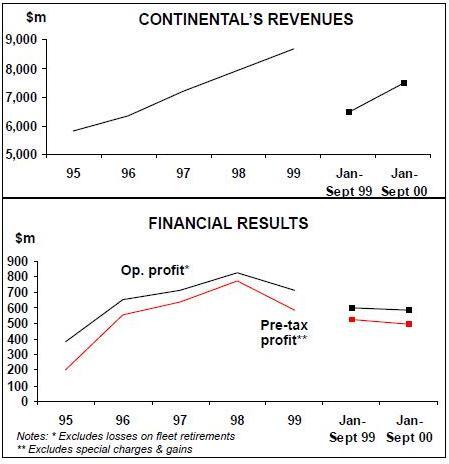

Since emerging from its second Chapter 11 visit in April 1993 and staging an impressive financial turnaround in 1995, Continental has achieved its target of a 10% operating margin every year. The profits have not been the industry’s highest, but they have been remarkably consistent in light of rapid international growth and a process of bringing wages to industry standards. The results for the latest period — an operating profit of $254m (up 26%) and a net profit of $135m (up 30%) for the quarter ended September 30 — represented 9.7% and 5.1% margins — among the industry’s best in a very challenging operating environment.

One of the most impressive things about Continental has been its ability to grow rapidly without adverse impact on the bottom line. In 1997–1999 its capacity surged by around 10% annually as it started building its "underdeveloped" hubs at Houston, Newark and Cleveland, which had spare capacity and a large potential local traffic base. However, growth slowed down progressively in 2000 to average a little over 5%.

This year’s is expected to be around 4.8% — or 3.2% if the impact of a new Hong Kong route is excluded. The lower rates in part reflect earlier–than–planned DC–10 retirements, though pressure on operating margins must have been a factor. The company has repeatedly assured the investment community that growth would continue only if the 10% operating margin can be maintained.

Another unique aspect about Continental is its continuously improving business mix — something that helped compensate for the adverse effects of rapid expansion. The business traveller content of its total traffic has risen steadily, from 37% of domestic passenger revenues in 1995 to 46.2% at present. The ultimate target is 55–60%, leaving another $100m or so upside potential.

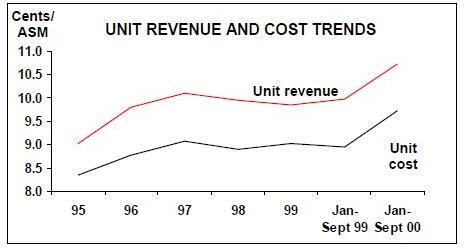

This trend manifests itself in large increases in average fares — for example, in the September quarter, Continental’s average fare rose by 8.8% despite a 77.5% load factor. Unit revenue growth was the industry’s second highest at 11%.

The rise in the business traffic content has reflected excellent customer service and continued high on–time performance and flight completion rankings. The fact that Continental led the industry by a large margin in on–time performance last summer could only be attributed to its stable labour relations.

Unit costs have been kept in check despite considerable wage pressure. This has resulted from fleet renewal, non–value added cost reductions, productivity improvements and — like the rest of the industry — significant distribution cost savings. Internet sales accounted for 7% of passenger revenues in the September quarter and continue to grow rapidly. Distribution costs are expected to decline from the current 14.5% of revenues to 7–10% by 2005, the aim being simply to keep up with the industry trend. Total unit costs rose by 9.3% in the latest quarter, or by 2.5% if fuel is excluded — both pretty much in line with the industry trend. Cost per ASM were 9.65 cents — considerably below United’s and American’s but higher than Northwest’s and Delta’s.

However, in light of the expensive labour disruptions experienced or now brewing at all of those carriers, Continental, with its stable labour situation, is much better positioned financially for the coming year than the other large network carriers.

Highly leveraged balance sheet

The company benefits from a management team that is regarded as the best in the US airline industry. Gordon Bethune, the current chairman and CEO, has been named one of the 50 best CEOs in America for two years running by Worth magazine’s survey of Wall Street analysts. His right–hand man Greg Brenneman, president and COO, has been a highly sought–after candidate for CEO position at large US corporations. CFO Larry Kellner has won "CFO Excellence Award" for three years running. Continental has what stock–market analysts describe as an "aggressive" financial policy — a reference to its high level of debt and continued substantial share repurchases. Because of that, its credit ratings are lower than AMR’s, UAL’s and Delta’s. However, despite continued heavy capital spending, there are no real concerns about the situation.

Long term debt and capital leases rose from $2.2bn in 1995 to $3.9bn at the end of September 2000, giving Continental a relatively high mid–80s debt–to–capital ratio. This has been the result of substantial fleet renewal, as well as aggressive share repurchasing, which has left less cash available to prepay debt. Nevertheless, the company insists that it has a "balanced" strategy, having prepaid about the same amount of debt as was used for share repurchases last year. It has also generally exceeded its cash target of $1bn — at the end of September cash reserves were $1.16bn.

Unlike its competitors, Continental continued extensive share repurchasing last year. By mid–October it had repurchased $1.19bn of stock under a programme authorised in 1998, with another $260m remaining. The policy is to repurchase amounts equal to half of its adjusted net income, all net proceeds from the sale of non–strategic assets and (since September) all cash proceeds to the company from employee equity incentive plans.

None of that, of course, has had much impact on the share price; rather, it has helped constrain potential upgrades in credit ratings. However, the resulting decline in Continental’s share count (also impacted by the share repurchase from Northwest) will mean strong growth in per–share earnings in both 2000 and 2001.

The current consensus estimates are a net profit, excluding special items, of $5.64 per share in 2000 and $6.65 in 2001, which would represent 15% and 18% annual increases. The actual earnings are expected to be flat for 2000 and decline this year (depending on fuel prices and the extent of the economic and business travel slowdown).

Fleet renewal and simplification

Continental’s general share repurchasing will now slow down because of the $450m buyback from Northwest, which is being partially funded through new debt, and because of another $1bn of aircraft financings completed in recent months. The company is in the process of rationalising and modernising its fleet, which in 1998 included nine different aircraft types covering virtually the full range of jets offered by Boeing. The number of types has now been reduced to six and is planned to go down to just four by 2003. Average fleet age has already declined from 13.4 years in 1994 to 8.5 years at the end of 1999.

This process is obviously leading to substantial cost savings. Continental, which is very poorly hedged for fuel this year (like much of the rest of the industry), is "putting a long term fuel hedge in the fleet", as Larry Kellner recently expressed it.

The plan has much flexibility built in to allow Continental to regularly review the growth rate, based on profit margins.

Currently the expectation is that the fleet will grow from 371 at year–end 2000 to 415 by the end of 2002, though anywhere between 370 and 437 is permissible in the plan. In two years' time, 70% of the fleet is expected to be common–rated 737s (300, 500, 700, 800 and 900 series). There are 15 737–900s on order for delivery from May. Continental also recently ordered 15 757- 300s, mainly for domestic service to supplement its 41–strong 757–200 fleet. The last of the 65 MD–80s currently in the fleet will retire in 2005.

The 777, introduced two years ago, is utilised in the key Asian nonstop markets and on some transatlantic sectors previously served with the DC–10–30. Deliveries of the 767–200ER and 767–400ER, which began in 2000, will enable the DC–10 retirement process to be completed in 2003.

Regional subsidiary Continental Express is expanding rapidly and moving towards an all–jet fleet over the next few years. It launched the 50–seat ERJ–145 in 1997 and the 137–seat ERJ–135 in 1999.

Stable labour situation

Continental continues to enjoy excellent labour relations, in part because of the ongoing process or restoring wages to industry standards. In June 1998 it essentially gave in on economic issues in difficult contract talks with the pilots. It also pays generous amounts in profit sharing and takes care to treat unionised and non–unionised employees equally. As a result, it has avoided further unionisation (still around 40%).

Not having any contracts amendable in 2001 is an enormous advantage in light of the contentious negotiations and associated labour disruptions many other US carriers currently have to deal with. The next contract to come up for renewal is one with the mechanics (IBT) in January 2002, followed by the pilots (IACP) in October 2002, dispatchers (TWU) in October 2003 and flight attendants (IAM) in October 2004.

That said, Continental’s management has agreed to open the pilot contract talks nine months earlier than planned — a full 12 months before the due date. IACP wanted an early start to make absolutely sure that a deal could be secured by October 2002 that matches or exceeds the large rises recently granted to United’s pilots and promised to Delta’s.

Getting the process and the timeline sorted out early was obviously a good idea.

Since the initial months will only see an exchange of proposals and the proper talks will not start until January 2002, there should be time to complete the mechanics talks.

The pilots have claimed that they are still substantially behind the rest of the industry in pay and benefits and that by October 2002 their pay will be as much as 62% below the industry’s top levels. They will seek to fully close the gap and will be in a better position to do so following the recent signing of a merger agreement between the boards of IACP and ALPA, which will be voted on by the pilots in March or April. While closing that gap will be a small price to pay if it means avoiding expensive work disruptions, a substantial hike in labour costs will obviously be the toughest issue facing Continental in the long term. However, it is not alone in facing that issue and, thanks to its good labour relations, may be able to maintain a productivity advantage.

Impact of the Northwest share buyback

Continental is in the process of buying back most of the Class A shares Northwest acquired from Air Partners in 1998. The earlier deal gave Northwest a board seat, 59.6% of the voting power (limited for an initial 10–year period) and rights to take full control of Continental in 2008 (with some of the limitations expiring in 2004). The two signed a definitive agreement on the repurchase in mid–November and the deal was subsequently approved by their boards.

The buyback and a subsequent recapitalisation will still have to be approved by Continental’s shareholders (January 22), but this will be a mere formality because Northwest holds majority voting power and is contractually committed to vote for the deal. Barring any delays in completing the paperwork, the transactions are expected to close by early February.

Despite some criticism that the deal is not good for other Continental shareholders, it is generally thought to represent a fair and reasonable compromise on a contentious governance issue. Northwest will receive $450m in cash, fully recovering its investment plus interest (Continental is paying a 29% premium over the previous day’s share price — virtually the same that Northwest paid).

The immediate benefit was to avert a prolonged court battle with the Justice Department, which could have had adverse effects on Continental’s highly profitable commercial alliance with Northwest. The DoJ has promised to drop the antitrust lawsuit against the airlines once the restructuring, which will reduce Northwest’s voting stake in Continental to 7%, is completed. Significantly, the deal made it possible to extend the alliance by ten years to 2025.

Now the two carriers can focus all attention on their commercial cooperation, which is expected to generate around $225m in pretax profits to Continental this year.

The deal will remove much of the uncertainty regarding Continental’s independence and future, which the company says has hurt morale. Continental had been keen to buy back the stake for at least a year. Now, for the first time since it emerged from Chapter 11 in April 1993, it will have no major shareholder whose interests might clash with those of its own.

Resolving this issue "increases the likelihood that our very successful management team will remain in place", the company said in an SEC filing.

It is worth bearing in mind the highly positive effects of a similar situation a few years ago, when Northwest repurchased a stake held by KLM. Severing the equity link rescued the two carriers' relationship and enabled them to extend and further develop their successful transatlantic alliance.

Just about the only possible concern about the deal is that Northwest will retain veto powers over any merger or change of control transaction involving Continental and another major carrier. It will be issued one share of a special series of B preferred stock for $100 for that purpose.

However, the deal does have provisions to ensure that Continental will have flexibility to respond if there is a new consolidation phase in the US industry. Northwest will lose the veto powers the minute it signs a merger deal (or any kind of transaction that involves buying or selling 25% or more of capital stock or voting power) with another major carrier. Also, there are new provisions in the alliance agreement allowing termination with six months' notice in the event of a change of control at either carrier.

Consequently, the blocking rights should not impede Continental’s progress. The Northwest alliance will give it most of the network benefits of mergers without the risk of expensive labour disruptions. And, since the veto powers only apply to airline mergers, the company will be able to consider any good offers from investor groups.

It could have been much worse. According to the SEC filing, the issue was apparently one of the main sticking points in the negotiations that lasted almost 12 months. Northwest had wanted blocking rights on a broad range of corporate transactions, as well as a "liquidated damages provision". This was not because it wanted to ever control Continental but because it feared making a long–term commitment to an alliance that, like the AMR–US Airways relationship, would unravel if someone else acquires Continental.

The recapitalisation, which will involve reclassifying each Class A share (carrying ten votes each) into 1.32 Class B shares (one vote), will abolish the two–tier voting structure — one of the most visible reminders of Continental’s Chapter 11 past.

Strong market position

The code–share/FFP alliance between Northwest and Continental creates a combined domestic network approaching those of the top three — American, United and Delta. In Continental’s words, it has "rounded out" a network that was already strong thanks to rapid growth at the hubs.

Growth at Newark has increased

Continental is the primary carrier at each of its four main hubs, accounting for 77% and 55% of average daily jet departures (including RJs) at Houston and Newark, 49% at Cleveland and 70% at Guam. Continental’s share of the New York City market from 16% in 1993 to around 26% in 2000 — largely at the expense of American, which has seen its share fall from 25% to 19%. Its position as the only major carrier to operate a hub for New York City, the world’s largest business travel market, gives it an important strategic advantage, though depending heavily on such a competitive market poses risks. JetBlue’s aggressive future growth plans from JFK are a point of concern.

Significantly, there is still potential to grow the main hubs when profit margins allow. And Continental is in a prime position to gain from any UAL/US Airways asset divestitures, having boldly made an early $215m bid for the Washington National assets that US Airways hopes to sell to DC Air.

Another positive is a relatively diversified international network by US carrier standards, which reduces the risk of being too badly affected by problems in any particular region. An already strong competitive position in Europe will be enhanced with more services from Newark and a gradual integration into the Northwest–KLM alliance. Latin America, where Continental is already the second–largest US carrier, will see continued expansion, as allowed by ASAs, and further development of alliances (currently with 49%-owned COPA, Aserca and Air Aruba). Asia will be boosted by the new New York–Hong Kong service this year, following the introduction of Tokyo routes a year ago.

Continental’s leadership has continued to repeat the argument that, because of the New York hub, the airline does not really need a European partner. This, of course, reflects a desire to operate nonstop services to as many cities as possible.

The current worldwide alliance network is considered to be essentially complete. The airline envisages the addition of just two more partners, to bring the total to 20 by 2005. However, there is still "a lot of systems work to do" to optimise the network and realise all the benefits.

| In operation | On order | Remarks | |

| 737-300 | 65 | ||

| 737-500 | 66 | ||

| 737-700 | 36 | 20 | Delivery 2001-02 |

| 737-800 | 58 | ||

| 757-200 | 41 | ||

| 767-200ER | 3 | ||

| 767-400ER | 4 | 30 | Delivery 2001-03 |

| 777-200 | 16 | ||

| DC-10-30 | 17 | All to be sold | |

| MD-80 | 65 | 45 to be sold | |

| Total | 371 |