Alitalia: Rinascimento

o Morte

Jan/Feb 2021

Four years ago, well before the onset of the coronavirus pandemic, Alitalia ran out of cash and was put into short-term emergency administration. It was given a government loan of €900m, to be repaid within six months. The idea was to allow the administrators time to find a buyer for the financially-challenged Italian flag-carrier.

And Alitalia has forever been financially challenged. As the chart shows, it has reported an operating profit in only two of the past 25 years (1997 and 1998) and a net profit (benefiting from asset sales) in only four.

It could have been good timing to find a buyer: the industry was profitable and on a continued upswing; and there seemed to be a lot of interest with suitors such as easyJet, Lufthansa and even Ryanair. Air France-KLM, having had its fingers burnt in previous restructurings, bowed out of the race but got its partner Delta involved — at the time on a roll of buying minority stakes in airlines round the world (including Air France-KLM) — to keep the airline in the Skyteam alliance and their immunised transatlantic joint venture.

But the cogs of Italian bureaucracy move slowly at the best of times, and were not helped by political infighting about the necessity of keeping the national flag-carrier in Italian hands. In the previous restructuring in 2013 four of Italy’s major banks (UniCredito, Banca Intesa Sanpaolo, Banca Popolare di Sondrio and Banca Monte Paschi di Senna) along with Atlantia (which runs Rome’s airports), the state-owned postal service Poste Italiane and national stalwart Pirelli had been persuaded to support the flag carrier. That paved the way for Etihad to invest €1.75bn for a 49% stake, sweetened by side deals including the sale of some of Alitalia’s Heathrow slots and a 75% stake in its frequent flyer programme MilleMiglia.

In the 2017 bankruptcy, all these players will have lost their equity investments, but in the attempt to find a new buyer, the government had the bright idea of getting the national railways involved (see Aviation Strategy May 2019) and the period of special administration was extended to allow Ferrovie dello Stato (FS) to develop a commercially realistic case for investment.

But FS could not justify holding more than 35% of the equity. The Italian Ministry of Finance felt it could take a 15% stake without incurring wrath from Brussels for providing illegal state aid. But by the end of 2019 it could not persuade Delta (who had just bought a 20% stake in LATAM for $1.9bn) to improve its offer of €100m for a 10% stake in the newest version of Alitalia, and it was left with a massive funding gap.

Then by March 2020, the first wave of Covid-19 pandemic devastating airline revenues worldwide, time had run out on the idea of ever finding a buyer. The Italian government announced that it would renationalise Alitalia.

By June 2020, it was said, a new state-owned company, Italia Trasporte Aereo (ITA), with €3bn of funding would acquire the “good” parts of Alitalia — the brand, the frequent flyer programme MilleMiglia (at the end of 2019 Alitalia had apparently bought back the 75% it had previously sold to Etihad), and the slots at Milan Linate — exactly what should have happened in the 2008 and then the 2013 restructuring — and relaunch the airline with a modestly smaller fleet (of 90 aircraft compared with the prepandemic 133). What would happen to the maintenance and ground handling units, employing 4,000 people, wasn’t made clear.

In doing so the government was perhaps emboldened by the ease in which Germany, France and the Netherlands had been able to pour in billions to support their flag-carriers; and the approval by the European Commission of Italy’s own provision of €199.45m in cash to Alitalia during the pandemic, judging that to be valid state aid.

The June deadline passed, and the relaunch of the new and improved Alitalia slipped through the rest of the year: there seems to have been broad consensus that Francesco Caio, an executive with a background in telecoms and banking and who led the postal service Poste Italiane to an IPO in 2015, should be the company’s Chairman and Fabio Lazzerini, a former general manager of Emirates and most recently Alitalia’s chief business officer, should take over as chief executive; but political infighting among the country’s fragile coalition government apparently failed to find agreement on other members of the board.

The plan resurfaced in January, with a new launch date for Alitalia ITA in April. This time the idea was to start up with an even smaller fleet of 50 aircraft, but rebuild operations back to over 100 aircraft over the following few years. As in all the previous restructurings, the business plan seems to target break-even within two years and a sustainable 8-10% operating margin thereafter.

But the architects of the plan had possibly forgotten that the Commission was still investigating the €900m “short term” government loan provided in 2017 and a subsequent €400m government grant in 2019, still to decide whether these contravened the Union’s state aid rules.

According to report in L’Espresso news magazine, the European Commission wrote to the Conte Government in January asking for guidance on the proposed plans. The leaked correspondence apparently expressed concern that the project as it stood was merely “a simple corporate transfer operation without discontinuity with the old company,” and stressed that the constituent parts of the old Alitalia should be split and sold separately through an “open, transparent, non-discriminatory, unconditional tender” to third parties, and not just transferred to the new nationalised entity in a private transaction.

And then at the end of January, with the fragile coalition collapsing, the Conte government resigned, paving the way for the appointment of a technocrat government led by former head of the European Central Bank, Mario Draghi.

Shortly after his appointment, Italian daily newspaper La Repubblica ran a story suggesting that because of Draghi’s “good relations” with Germany and Angela Merkel, Italy was now investigating another exit route for the flag carrier. The idea promulgated was to put the Alitalia airline operations into the company’s regional subsidiary CityLiner, hand it over to the Ministry of Finance, and persuade Lufthansa to buy it — in the same way that Lufthansa had invested in the resurrections of Swissair (through Crossair, renamed Swiss) and Sabena (through its regional subsidiary DAT, renamed SN Brussels).

The article failed to mention that Lufthansa had waited for Swiss to become profitable (and the Swiss government to renegotiate all its bilateral air service agreements) before taking a majority; reluctantly acquired a majority in Brussels Airlines before it could produce a profit; and is specifically precluded from making acquisitions under the terms of its €9bn bailout from the German government in 2020. It also has its own existential crisis.

Italian flag dilemma

The political will is to maintain a national flag-carrier (and incidentally safeguard at least some of 10,000 jobs in a highly unionised workforce). After signing the decree published last year to create the new ITA, transport minister Paola de Micheli said, “a national airline is born that will have to play a leading role on the European and international market... a large industrial operation at the service of the country, in support of the competitiveness of our businesses and the relaunch of Italian tourism”.

But the political will ignores the commercial realities, and the legacy of Alitalia’s failure to react to the development of the air transport industry since deregulation.

It had emerged from the 2008 bankruptcy two-thirds the size of its former self — and that was after an effective merger with Air One. Since then Alitalia had hardly grown at all — and this in an industry that depends on long term growth to stand still. Its share of the Italian short haul market fell ten points from 30% to 20% leaving it in 2019 well behind market leader Ryanair, and just ahead of easyJet.

| Route pair | Seats (000s) | Daily flights | Dom | Eur | Int |

|---|---|---|---|---|---|

| Milan-Rome | 1,705 | 19 | • | ||

| Catania-Rome | 1,357 | 11 | • | ||

| Palermo-Rome | 1,019 | 8 | • | ||

| Cagliari-Rome | 839 | 7 | • | ||

| Catania-Milan | 718 | 7 | • | ||

| Rome-Venice | 716 | 6 | • | ||

| Rome-Turin | 689 | 6 | • | ||

| Cagliari-Milan | 672 | 6 | • | ||

| Bari-Rome | 667 | 5 | • | ||

| Lamezia-Terme-Rome | 615 | 5 | • | ||

| Milan-Naples | 605 | 7 | • | ||

| Bari-Milan | 538 | 6 | • | ||

| Genoa-Rome | 535 | 5 | • | ||

| Paris-Rome | 530 | 4 | • | ||

| Rome-Tel Aviv | 522 | 4 | • | ||

| Milan-Palermo | 515 | 5 | • | ||

| Brindisi-Rome | 509 | 4 | • | ||

| New York-Rome | 494 | 3 | • | ||

| London-Rome | 460 | 4 | • | ||

| Naples-Rome | 445 | 4 | • |

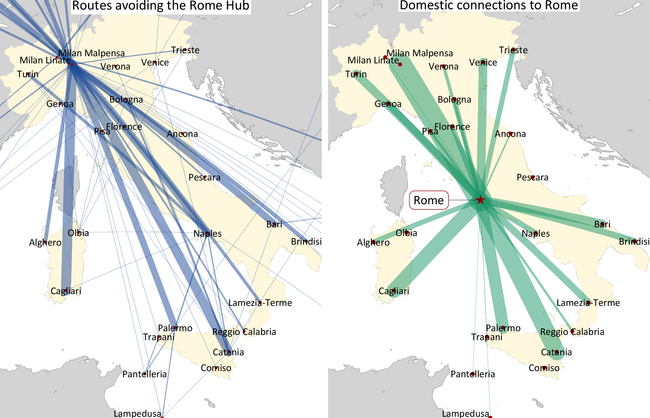

Half of its total seat capacity in 2019 was accounted for by twenty routes — all but four domestic (see table) — the first international route, that of Rome to Paris, coming in at number 14. Moreover, six of the top twenty routes avoid the hub in Rome entirely. Indeed as the map shows, Alitalia operated a large number of point-to-point routes that avoided Rome; and a reasonable number of thick routes centred on Milan Linate — the northern city’s convenient but constrained downtown airport at which Alitalia holds over 60% of the slots.

In the current restructuring plan Alitalia has suggested that it will eliminate all “hub-bypass” routes lacking international connections (supposedly such as Turin to Sicily — which it doesn’t actually fly). Presumably it will retain its network of point-to-point routes to Milan, and has said it would leverage the “negotiating power” of its superior portfolio of slots at Milan-Linate through a deal with Air France or Lufthansa (or anyone else?).

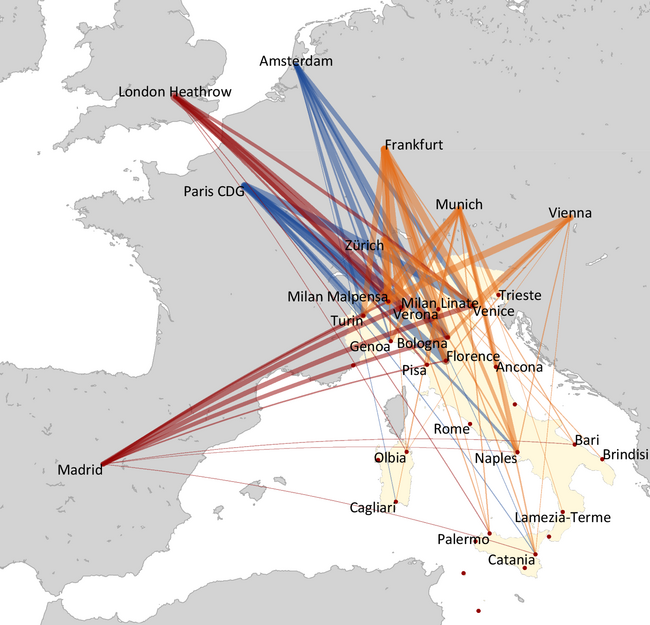

The real dilemma is that Italy is really two disparate countries within one. The north, and particularly the Po valley, is the wealthy industrial area. The south — the Mezzogiorno — is a relatively impoverished area with regional annual per capita incomes less than half that of the North. The industrial north is centred in Milan; the political centre is in Rome. There are strong traffic flows between them undermined by the development of high speed rail.

Italy, like the other mediterranean countries, is a tourist destination. Inbound tourist traffic is intent on reaching the leisure destinations, well away from the industrial or political centres: highly seasonal and price oriented.

However, there is also strong demand from the Po valley on longer haul routes, and this (without having to go through Milan) is easily diverted to feed the major European hubs (see map) each of which able to offer more numerous and convenient connections supported by underlying O&D demand than Alitalia at Rome.

Note: thickness of lines directly relate to number of daily flights

In all the confused discussion of the restructuring plan, no-one seems to address the fundamental question of quite where Alitalia makes its losses: Milan, Rome, regional, or long haul.

| In service | Parked | Total | Avg Age | |

|---|---|---|---|---|

| A319 | 20 | 2 | 22 | 13.8 |

| A320 | 5 | 33 | 38 | 14.1 |

| A321 | 1 | 4 | 5 | 22.0 |

| A330 | 3 | 9 | 12 | 11.4 |

| 777 | 6 | 6 | 12 | 17.2 |

| ERJ170 | 8 | 2 | 10 | 8.8 |

| ERJ190 | 4 | 1 | 5 | 9.2 |

| Total | 47 | 57 | 104 | 13.7 |