Chinese Big Three:

2016 update

Jan/Feb 2017

The CAAC has just produced another series of epic results for the Chinese aviation industry — total passenger traffic volume in 2016 was up by 11.8% to 488m, 436m “domestic” (which includes 10m to Greater China: Hong Kong. Macau and Taiwan) and 52m international. International expanded by 22.7%, domestic by 10.7%.

The economic background appears to be remaining strong. 2016 GDP growth was 6.7%, which is down on the 10%-plus levels of a few years ago but the authenticity of those super-growth rates has been questioned, and the conclusion is that they were almost certainly inflated. Looking forward the Chinese government is targeting 6.5-7.0%pa GDP growth, with an increasing focus on domestic consumption.

Recent developments at the Big Three — Air China, China Eastern and China Southern, which together account for about three quarter of the Chinese industry are reviewed below.

The economic background appears to be remaining strong. 2016 GDP growth was 6.7%, which is down on the 10%-plus levels of a few years ago but the authenticity of those super-growth rates has been questioned, and the conclusion is that they were almost certainly inflated. Looking forward the Chinese government is targeting 6.5-7.0%pa GDP growth, with an increasing focus on domestic consumption.

Recent developments at the Big Three — Air China, China Eastern and China Southern, which together account for about three quarters of the Chinese industry are reviewed below.

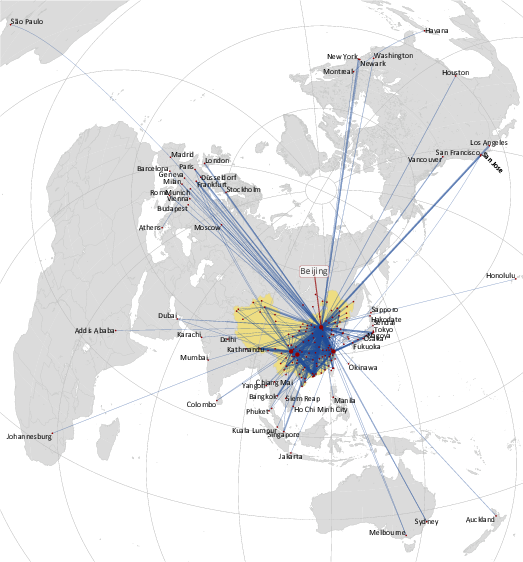

Air China

China’s flag carrier is based in Beijing and operates more than 360 routes to around 180 destinations in 40 countries, of which 108 are domestic. Altogether the Air China Group employs more than 50,000, of which the majority work at the mainline.

In the first three-quarters of 2016, revenue at the Air China Group rose 3.7% to RMB85.4bn (US$12.7bn), based on a 4% rise in passengers carried to 44.4m. Operating profit increased 21.2% in the period to RMB9.6bn ($1.4bn) and net profit was up by 15.1% to RMB7.2bn ($1.1bn). In January-September 2016 the overall Air China group saw total ASK growth of 9.3% beaten by RPK growth of 9.8%, leading to a 0.37% rise in passenger load factor, to 80.9%.

For the mainline Air China, ASKs and RPKs both rose by 8.2% over Q1-Q3 2016 with load factor static at 80.5%. Air China has the highest proportion of international traffic of all the Big Three, and this share grew in the first three-quarters of 2016 as international RPKs rose by an impressive 17.1%, substantially ahead of traffic growth on domestic routes (2%), and on regional routes (defined as Hong Kong, Macau and Taiwan, and where traffic fell 5.2% year-on-year).

Air China is still ahead of its Big Three competitors in terms of international traffic. International RPKs as a proportion of all RPKs grew to 34.8% in 2016 (compared with 33.9% at China Eastern and 28.2% at China Southern). This has risen from a proportion of international traffic at Air China of 31.0% just two years previously, (when China Eastern had a 27.4% international share and China Southern a 20.9% share) as Air China pursues a strategy of prioritising international growth and increasing load factor on — and utilisation of — its widebody aircraft.

Digging deeper into the numbers, that international growth varied considerably by region. In 2016 traffic to/from Europe increased by 5.5%, but this was behind growth of 16.1% to North America and 19.3% to Japan and Korea — and significantly behind a 43.6% rise in traffic to south-east Asia and other regions.

Air China’s mainline fleet has expanded significantly over the last few years, from just over 300 aircraft in 2014 to 379 today (of which just under 40% are owned outright) — though this is still the smallest mainline fleet among the Big Three.

That mainline fleet includes 145 737s, 133 A320 family aircraft, 55 A330s, 29 777s, 10 747s and seven 787s. They have an average age of around six and a half years, with 33 A319s having the oldest age profile (just under 11 years), followed by the 747s (eight years — though has reduced significantly, from an average age of more than 18 years in 2014 as new 747-8s have joined the fleet). If subsidiaries such as Air China Cargo, Shenzhen Airlines and Air Macau are included, the Air China group fleet comprises more than 600 aircraft.

On firm order at the mainline are 162 aircraft, comprising 66 737-800s, 33 A320neos, 15 A320-200s, 10 A350-900s, 10 A330-300s, eight 787-9s and 20 Comac C919s. These orders will both expand the fleet and replace ageing aircraft.

Air China’s international strength is underpinned by its dominance at Beijing, a key benefit of being the nation’s flag carrier. Other advantages of its favoured status have included being merged with much stronger domestic airlines (than have been government-mandated for China Southern and China Eastern), and being awarded a huge amount of official government travel.

The airline has also been building up hub operations at Chengdu and Shanghai, the former primarily as a domestic hub and the latter as both a domestic and international gateway, with a focus on increased frequencies on trunk routes and better connectivity and transit capabilities.

Air China is continuing its strategic partnership with Cathay Pacific Airways (in which it has a 29.9% stake, while Cathay has a 20.1% stake in Air China), though its most notable alliance development in 2016 was the conclusion of two years’ negotiations with fellow Star member Lufthansa, the result of which is a joint venture between the two on routes linking China and Germany, which will go into effect in summer 2017.

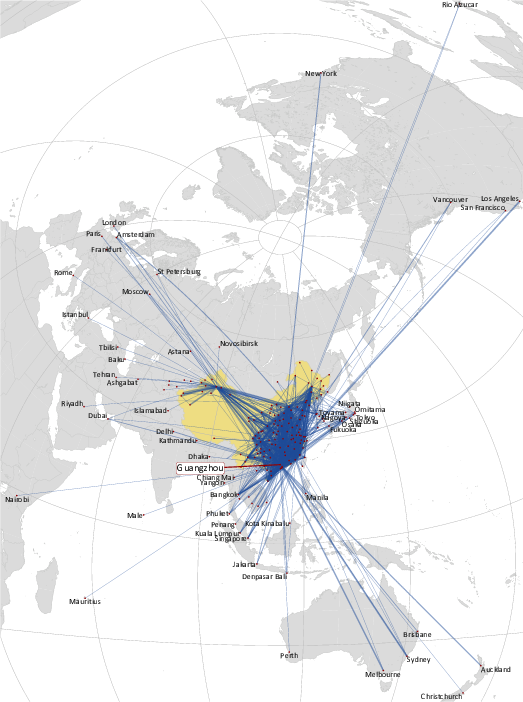

China Southern

Guangzhou-based China Southern operates to 208 destinations in 40 countries, of which 125 are domestic. The group employs around 90,000, of which just under 70,000 work at the mainline, and it’s still the largest of the Big Three — whether measured in terms of its fleet, traffic or revenue. As well as its prime operation at Guangzhou, China Southern has developed domestic hubs at Chongqing (in the south-west of China) and Ürümqi (in the north-east), and an international hub at Beijing, in competition against the flag carrier.

China Southern is still China’s leading domestic airline by far, with 70.3% of its RPKs in 2016 coming from domestic traffic (compared with 63.5% at China Eastern and 61.5% at Air China over the same period).

However, that percentage has fallen from the 77.2% proportion of domestic traffic China Southern had two years ago, as the carrier has been prioritising international expansion (particularly to Europe and North America). Last year ASKs grew by 22.8% on international routes (with RPKs growing by 22.7%), compared with just a 4.4% capacity increase domestically (4.5% RPK growth) and a 12% fall in regional ASKs (with a 12.6% decline is RPKs).

In the first three-quarters of 2016 China Southern’s revenue rose just 1.5% year-on-year to RMB86.7bn ($12.9bn) thanks to a 2.9% rise in passengers carried in the period to 85.6m. In the January-September 2016 period China Southern’s ASKs growth of 8.1% was not quite matched by RPK growth of 7.5%, resulting in a 0.46% fall in passenger load factor, to 80.6%.

At the operating level profits rose 30.9% in Q1-Q3 2016 to RMB6,995m ($1,043m), and at the net level profits increased by 30.4% to RMB7,535m ($1,124m).

Whether at a mainline or group level, China Southern has the largest fleet of any of the Big Three carriers. The mainline operates a fleet of 521 aircraft, comprising 247 A320 family, 167 737s, 38 A330s, 25 757s, 10 787s, seven 757s, five A380s, two 747s and 20 ERJ-190s. They have an average age of just over seven years, with the oldest aircraft being the 757s, which has an average age of more than 18 years and which reportedly are being sold back to Boeing. With subsidiaries, the China Southern group has a fleet of more than 700 aircraft.

On order at the mainline are 183 aircraft: 98 A320neos, 27 A320-200s, 16 A330-300s, 12 787-9s, 10 A321s and 20 Comac C919s. The 787-9s were ordered in October 2016 and are worth around $3.2bn at list prices; China Southern was the launch customer for the 787, and the 10 787-8s in its fleet have operated successfully on long-haul routes from Guangzhou to destinations such as London, Rome, Vancouver and Christchurch. In January 2017 China Southern received the first of 24 A320neos being leased from AerCap, and which will be delivered over the period to 2019; in doing so China Southern became the first airline in China to operate the model.

Last year China Southern was reportedly interested in acquiring some of Air New Zealand’s 25.9% stake in Virgin Australia, which would have helped protect China Southern’s position as the largest carrier between China and Australia (it increased its flights to Australia by more than a third in 2016). Instead a 19.9% share was sold to Chinese conglomerate the Nanshan Group, which owns Qingdao Airlines, a small carrier based in the eastern Shandong province. More worryingly for China Southern, in 2016 the HNA Group (the owner of Hainan Airlines, the fourth largest carrier in China) acquired a 13% stake in Virgin Australia, which has subsequently risen to 19.9%.

Part of the SkyTeam alliance, China Southern has now turned its attention westwards, and is talking with Air Kyrgyzstan on a potential joint venture that would modernise the tiny carrier — though that deal is not exactly on the same scale as Virgin Australia.

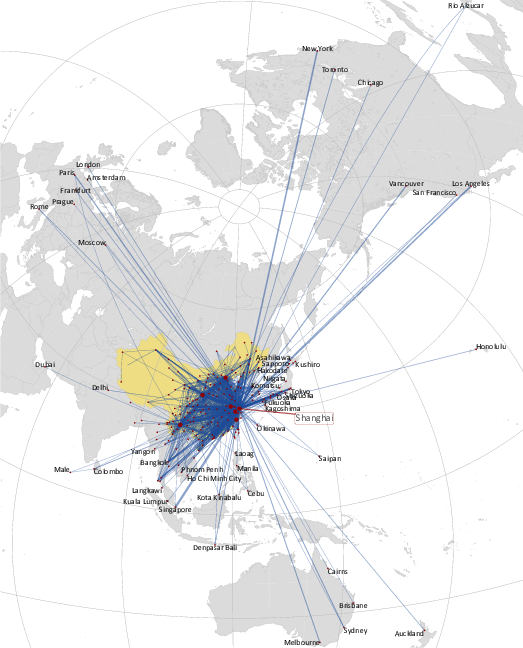

China Eastern

China Eastern employs more than 72,000 at a group level and currently operates to 78 domestic and 61 foreign destinations.

In January to September last year China Eastern recorded a 4.8% rise in revenue to RMB75.4bn ($11.2bn), with passengers carried in the period rising 8.2% to 76.3m. In Q1-Q3 2016 capacity growth of 13.7% was outstripped by a 14.4% rise in traffic, leading to a 0.5% increase in load factor, to 81.7%. In the first three-quarters of 2016 China Eastern saw operating profits increase significantly — by 59.7% to RMB5.5bn ($0.8bn) — while net profit rose 24.7% to RMB7.3bn ($1.1bn).

China Eastern’s mainline fleet comprises 452 aircraft — 266 A320 family aircraft, 125 737s, 45 A330s and 16 777s. The overall group fleet is approaching 600 aircraft. The airline has significantly fewer models than its Big Three rivals, and that’s the result of ruthless model pruning over the last few years. At under five and a half years, the mainline fleet has the youngest average fleet among the Big Three; the model with the eldest profile at China Eastern is the A320, with its 164 aircraft having an average age of less than seven years.

The mainline order book totals 228 — 70 A320neos, 59 A320-200s, 39 737-800s, 20 A350-900s, 15 787-9s, four 777-300ERs, one A321-200 and 20 Comac C919s. Last year China Eastern placed an order for 15 787-9s and 20 A350s that were worth more than $10bn at list prices, and due for delivery between 2018 and 2022. They will form the future backbone of China Eastern’s long-haul fleet, and will gradually replace older A330s.

And whether it likes it or not, under a government mandate China Eastern is likely to become the launch customer for China’s Comac C919 jet. The model is due to have initial test flights this year and be ready for delivery in late 2018 — although that delivery date has been pushed back repeatedly. And executives at China Eastern (and the other Big Three airlines) are likely to view the model as an unwanted distraction within their overall fleet modernisation plans.

In terms of financial results China Eastern is still the smallest of the Big Three, and in very simple terms that’s a result of being an “all-rounder” — it has neither the domestic strength of China Southern nor the international network of Air China. In 2016 its share of the Big Three’s combined mainline domestic capacity was 29%, and of international capacity 31.5%. But like its Big Three rivals, China Eastern faces intense competition domestically (leading to yield decline) and is prioritising international expansion, and in 2016 capacity grew by 28.8% on international routes (with RPKs growing by 29.6%), compared to just a 7% capacity increase domestically (8.2% RPK growth).

China Eastern is based at Shanghai (at both Hongqiao and Pudong airports) and has developed secondary domestic hubs at Kunming and Xi’an in the face of increasing competition at Shanghai from Air China and other carriers. In the first half of 2016 China Eastern’s market share at its hub airports were 40.5% at Shanghai (both airports combined), 37.3% at Kunming and 28.2% at Xi’an.

But China Eastern is also counter-attacking Air China through the continued growth of LCC subsidiary China United Airlines, which is based at Beijing’s Nanyuan airport and operates eight 737-700s and 25 737-800s to around 20 domestic airports — and which is reported to be very profitable.

Delta holds a 3.6% stake in China Eastern and the two carriers have been trying to improve connectivity between their networks. China Eastern is also endeavouring to increase ties with other SkyTeam members. For example, in July last year, it agreed a joint venture with Air France-KLM, which includes codesharing on each other’s Amsterdam-Shanghai Pudong services. China Eastern is also looking outside the alliance for further revenue-enhancing opportunities, and in August 2016 signed a codesharing agreement with British Airways on internal Chinese and UK flights.