Delta Airlines: liquidity problems looming

April 2004

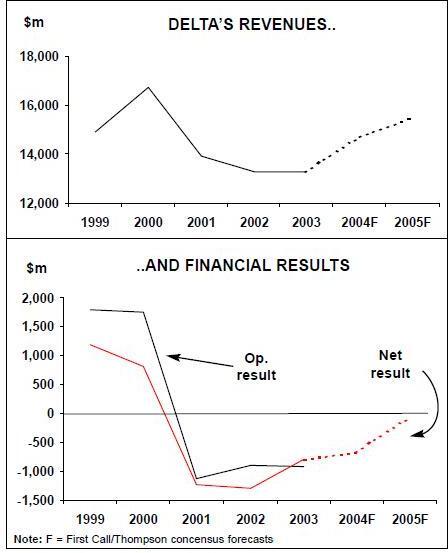

Delta’s financial position has deteriorated significantly in the past 12 months or so — something that previously went relatively unnoticed amid all the dramas at AMR, UAL and US Airways. The third largest US major faces heavy debt maturities and pension obligations this year. It has a significant exposure to LCCs; yet its unit costs are now probably the industry’s highest on a stage length–adjusted basis. Can these problems be solved without Chapter 11? Delta entered the current industry crisis in great financial shape. In the five years up to and including 2000, it had earned double–digit annual operating margins and net profits in the region of $1bn each year. Unlike many of its competitors, it had retained a low unit cost structure (while also improving unit revenues) in the boom years of the late 1990s.

The low cost structure was the result of the famous (and much–maligned) 1994–96 "Leadership 7.5" project, which slashed operating costs by $1.6bn and made Delta the lowest–cost major network carrier in the US. The project had to be abandoned early because of the more pressing need to restore service quality and employee morale. But a favourable four–year pilot contract in April 1996, low–fare subsidiary Delta Express (October 1996) and tight cost controls helped keep unit costs at an enviable 8.80–8.90 cents per ASM through to the end of the decade.

Because of the mid–1990s restructuring, Delta also had a strong balance sheet and investment–grade credit ratings.

Consequently, it was able to continue to tap the capital markets for funds to a much greater extent than other large network carriers after September 11, 2001, despite losing just as heavily in 2001 and 2002. It has completed a variety of financings, including privately placed EETCs. Last year it refinanced most of its 2003 debt maturities.

However, since early 2003 Delta’s financial recovery has essentially stalled. Its loss margins have been among the worst in the industry in recent quarters. While most other US airlines reported at least some improvement in 2003, Delta’s results worsened.

Excluding special items, it posted a $1bn net loss for 2003 (7.8% of revenues), after losing $958m in 2002. Last year’s operating loss before restructuring charges was $916m — also larger than the previous year’s $904m loss.

The main problem has been a surge in unit costs: from 8.80 cents in 1999 to 9.30 cents in 2000, 10.14 cents in 2001, 10.03 cents in 2002 and 10.58 cents in 2003 (all excluding restructuring charges). In this four–year period, CASM rose by 20% while RASM was essentially unchanged (down slightly from 9.97 to 9.90 cents).Delta has not only lost its CASM advantage but may have become the highest–cost large network carrier in the US. Its top executives are claiming that its stage length adjusted CASM is now even higher than that of US Airways — rhetoric that is obviously aimed at labour, but the claim may well be true.

Delta blames the problem squarely on its pilot costs, which are now totally out of line with its competitors. This is mainly due to the unlucky timing of past pilot contracts and extraordinary developments at competitors, but the implications are potentially serious.

Because of the continued heavy losses and substantially increased debt load, Delta has lost the competitive advantage it previously enjoyed in terms of balance sheet strength. The past winter has seen a steady stream of downgradings of its credit ratings — most recently by Fitch on April 7 and by S&P on March 17. As a result, Delta will find it harder (if not impossible) to access the capital markets and its borrowing costs may increase.

In the absence of pilot concessions, Delta’s financial situation will continue to deteriorate. S&P noted that "Delta will likely continue to report the heaviest losses among US airlines, consuming cash and undermining its already weakened balance sheet".

At the end of March, the First Call consensus forecast for Delta was a net loss before special items of around $660m in 2004, followed by a $63m loss in 2005. While these figures may change significantly depending on fuel price fluctuations, they nevertheless suggest that Delta has little chance of returning to profitability even in 2005. Delta has hedged 32% of its anticipated 2004 fuel needs at an average price of 76.5 cents per gallon — a relatively weak position, though many competitors are even worse off.

What makes Delta particularly interesting at present is that, more than any other network carrier, it represents both opportunity and risk to investors. After under–performing the industry for the past 12 months, its share price has excellent appreciation potential if and when a new pilot deal is announced. But if the labour talks drag out, Delta’s weakening liquidity and high cost levels make it vulnerable to prolonged adverse industry fundamentals.

To add to the uncertainty, Delta is in the process of digesting several leadership changes. First, Leo Mullin stepped down as CEO at year–end and was replaced by Gerald Grinstein, a longtime board member and a former CEO of Western Airlines and Burlington Northern (a railroad company).

This month Mullin will also retire as chairman, to be replaced by Jack Smith, a board member and former chairman/CEO of General Motors. On April 1, Fred Reid stepped down as president/COO to take up the CEO’s position at Virgin’s planned US domestic airline; Grinstein was expected to initially assume his responsibilities.

Grinstein’s first major move was to order a full strategic assessment of Delta’s business plan — due to be completed by July and presented to the board that month.

The need for pilot concessions

Otherwise, Delta’s priorities are to secure cost concessions from its pilots, meet this year’s debt and pension obligations, decide on low–fare unit Song’s future and, in the longer–term, address the heavy debt load. Delta has a pilot cost problem because it has been unlucky in two respects.

First, it happened to be the last major carrier to sign an expensive pilot deal before September 11. The contract was negotiated in the wake of United’s previous industry–leading deal, and it made Delta’s pilots the highest–paid in the industry.

Second, because Delta’s balance sheet was still relatively strong in 2002 and 2003, it could do nothing but watch helplessly as United and American, in their Chapter 11 and near–Chapter 11 situations respectively, extracted significant cost concessions from their pilots last year. In other words, Delta happened to be financially strong at precisely the wrong point in the industry (pilot contract) cycle.

It is worth noting, however, that Delta does not have a general labour cost problem. Only 18% of its employees are unionised (mainly pilots). There is considerable work rule flexibility among the nonunion workforce. The management estimated recently that Delta had a $600m non–pilot employee productivity advantage over competitors last year (the figure includes the impact of technology initiatives).

Much of that non–pilot labour cost advantage has been gained since September 11.

However, there have been no pay reductions (except for management); 70–80% of the improvement came from non–pocket book issues such as work processes. All worker groups continue to earn top–tier wage rates.

But pilots are extremely highly paid workers and the scale of the cost disadvantage there is staggering. Delta estimates that its pilot cost per block hour of $527 compares with an industry average of $315. Its pilots are paid 59% more than American’s and 82% more than United’s. Had Delta’s pilot cost structure been similar to competitors' in the fourth quarter, it would have posted a $120–220m lower net loss or almost broken even.

Delta has been in dialogue with its pilots since February 2003. It initially proposed cutting hourly wages by 23% and cancelling scheduled 4.5% pay increases in 2003 and 2004. It also asked for flexibility to start negotiations early on the entire contract, which becomes amendable in May 2005.

But there has been no progress. The pilots have offered to take a 9% pay cut and forgo the scheduled increases, while the management now has a 30% pay–cut request on the table. The talks have been at an impasse since January, though recently there were reports that some pilots are calling for the union to unilaterally decline the 4.5% wage increase scheduled for May 1 to help restart negotiations.

The management has a very strong case and there is little doubt about the eventual outcome: Delta will secure a cost–saving pilot contract. However, many analysts feel that getting that deal could take another 12 months. This is because Delta is nowhere near Chapter 11. Also, Grinstein has indicated that he is not prepared to accept a package of lesser short–term concessions.

Realistically, however, Delta will not be able to negotiate concessions that are anywhere near as deep as what American and United achieved in or near bankruptcy.

Delta pilots' pay rates are likely to remain the highest in the industry, though productivity improvements may help reduce the overall pilot cost disadvantage.

That said, a quick deal and deeper concessions are possible under some scenarios. First, the pilots may realise that the longer the delay, the deeper the concessions are going to have to be (as Delta’s financial condition deteriorates).

Second, there could be some specific adverse event that requires a quick pilot deal. For example, Delta might suddenly find itself unable to raise needed capital if banks and investors began to worry about the cost issues.

Grinstein has continued to insist in recent speeches that a pilot deal before July is possible. He has persistently hammered the point that if there is a switch from "mid–contract" to "new contract" negotiations, the number that is on the table will have to be larger (he is more experienced with unionised labour than Mullin was). However, if there is no deal by August, it will then probably have to be a new contract negotiation.

In the meantime, Delta continues to press on with cost cutting in other areas. There is a broad–based plan to save $2.5bn or reduce non–fuel unit costs by 15% by the end of 2005 (over year–end 2002 levels).

A few months ago the airline was talking about 8.5 cents being the CASM goal before pilot concessions. Delta claims to have achieved $1.2bn of the targeted $2.5bn cost or revenue initiatives in 2003, though the net gain (after offsetting cost pressures) was only $700m. However, none of that was reflected in 4Q CASM, which rose marginally even when fuel was excluded.

What role will Song play?

Delta has a strong business franchise, with solid market positions in North America and on the transatlantic (82% and 13% of its total revenues, respectively).

Its positive attributes include a powerful hub at Atlanta, unbeatable RJ feeder operations (Delta Connection), Delta Shuttle, a marketing alliance with Continental and Northwest, and SkyTeam and other foreign airline alliances. Like other large network carriers, Delta may need to rethink some of its hub operations.

Like the rest of the industry, it could probably benefit from scaling back its 2004 growth plans; it is currently still aiming for 8.5% mainline ASM growth this year (6.9% domestically, 13.9% internationally).

But those are the sort of things that are probably part of the regular planning process anyway. It is not clear why Delta needed to launch a special review of all aspects of its operations (Grinstein did not exactly have to learn about it since he had been on the board). The project might have just been called "reassessment of Song".

Delta needs to think out the Song/LCC strategy very carefully because, like US Airways, it has unusually heavy exposure to low–cost carriers (about 70% of its revenues).

It feels particularly vulnerable, first, because of its strong Northeast–Florida presence and, second, because of its heavy reliance on connecting traffic.

Song was launched in April 2003 as a new low–fare unit to replace Delta Express primarily in East Coast and some transcontinental markets. Its purpose was to help Delta compete more effectively with LCCs through larger aircraft, high–frequency flights, advanced in–flight entertainment technology and innovative product offerings. It was both modelled on and targeted at jetBlue. The aim was to get unit costs 20% below Delta’s mainline 757s — through increased productivity of people, aircraft and other assets, rather than separate lower pay scales.

It is important to remember that Song has only just completed its first quarter of full–scale (36–aircraft) operations, so up to this point it has not been possible to assess how successful it is. But it has obviously not lived up to expectations since Delta put the unit’s much–anticipated New York expansion on hold in January.

At a recent JP Morgan conference, Grinstein referred to Song as a "fighter brand", saying that it is sometimes worth making an economic investment in order to hold off competition. "But there is always the question of the price you're willing to pay", he added. "We simply have to understand that better before we expand or make any changes."

On the negative side, comparisons carried out late last year by Raymond James analyst James Parker indicated that Song was performing very poorly in terms of load factors and fare levels on routes where it competed directly with jetBlue (though that was probably too early for a fair comparison).

Also, Delta appears to be falling seriously behind the other large network carriers in total RASM. According to 4Q length–of–haul adjusted RASM figures presented by Continental at a recent conference, Delta’s RASM of 7.22 (adjusted to Continental’s length of haul) was way below the industry average of 7.70 (American’s was 8.37 and Southwest’s 5.22). Merrill Lynch analyst Michael Linenberg said recently that he believed Song was part of the yield problem. On the positive side, there are all the operational innovations and efficiency improvements achieved with Song that are being migrated into the rest of the airline.

In particular, the Song experience has helped boost aircraft utilisation (through faster turnarounds, loading passengers differently, managing the gate process differently, etc.).

Liquidity and balance sheet issues

Delta has little near–term risk of bankruptcy because of its good liquidity position, namely unrestricted cash reserves of $2.7bnat year–end. The strong cash position is the result of various financings and the sale of stakes in Worldspan, Orbitz and Hotwire last year.

However, the cash position is expected to decline this year due to substantial financial obligations. The extent of the decline will depend on how much new funding Delta decides to or is able to raise. It had a promising start in February when it completed a $325m private offering of convertible bonds.

The convertible bond offering was an ideal method for Delta since it will not add to debt in the longer term. The airline took on $2.3bn of new debt in 2001, $2.6bn in 2002 and $2.2bn in 2003. It had $12.6bn in total debt and capital leases at year–end, plus $8bn of minimum operating lease commitments.

Its lease–adjusted debt–to–capital ratio was 103% — shockingly high but not out of line with the industry average.

Delta faces $1bn of debt maturities in 2004, of which $300m is interim RJ financing likely to be replaced by permanent financing.

This year’s total pension plan funding obligations are estimated at $450m. Capex is $1.2bn, half of which is for aircraft (mostly RJs which already have financing in place).

There are no available lines of credit and little in terms of attractive unencumbered aircraft that could be used as collateral in secured financings. However, fully owned regional subsidiaries Comair and ASA are attractive assets that could be monetised.

On the positive side, Delta’s credit facilities do not contain any negative covenants.

Also, large portions this year’s debt and pension obligations were already met in the first quarter. Fitch estimates that the impact was to reduce unrestricted cash to about $2bn at the end of March but that further erosion this year is unlikely.

All eyes now focus on 2005, which is not looking good at all for Delta. Debt maturities, capex and pension funding will all be higher next year. In the absence of pilot concessions and after another winter season, the airline could face serious liquidity pressures in the spring of 2005.

| 737-200 | 51 |

| 737-300 | 18 |

| 737-800 | 57 |

| 757-200 | 96 |

| 767-300 | 28 |

| 767-300EREM | 59 |

| 767-400EREM | 21 |

| 777-200 | 8 |

| L1011 | 26 |

| MD 11 | 13 |

| MD 80 | 120 |

| MD 90 | 16 |

| Total | 528 |